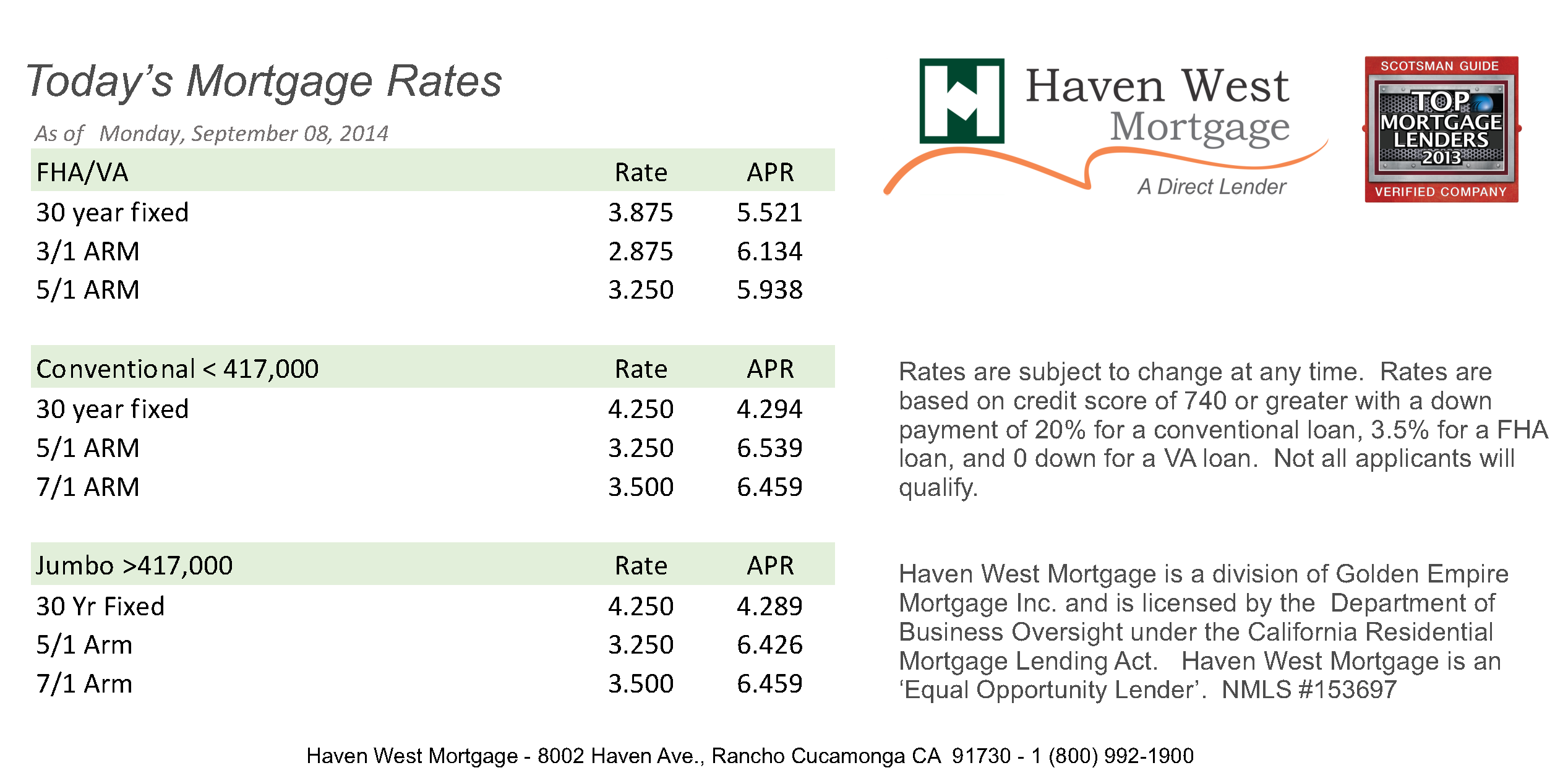

If you’re staring at a Zillow listing right now or checking your bank balance for the tenth time this morning, you probably want a straight answer. Honestly, the housing market has been a roller coaster, and trying to pin down exactly what is mortgage interest rates today feels like trying to catch smoke.

As of Saturday, January 17, 2026, the national average for a 30-year fixed mortgage is sitting right around 6.11%.

Wait.

Don't just take that number and run. If you look at Zillow, you might see 5.99%. If you check Bankrate’s APR survey, you'll see 6.18%. Why the gap? Because "the rate" isn't a single thing. It’s a moving target influenced by everything from your credit score to a random post on social media by the President.

The big news this week? We actually hit a three-year low. Just a few days ago, mortgage rates dipped significantly after President Trump directed Fannie Mae and Freddie Mac to buy up $200 billion in mortgage-backed securities. It was a shock to the system. One day we're coasting, the next, the bond market is scrambling.

The Real Numbers for January 17, 2026

You’ve got to look at the breakdown to see where you actually fit. Most people fixate on the 30-year fixed, but that’s not always the best move depending on how long you plan to keep the house.

For a 30-year fixed mortgage, the interest rate is roughly 6.11%, while the APR is closer to 6.18%.

If you’re looking at a 15-year fixed, you’re in a better spot. Rates there are averaging 5.47%.

Thinking about a refi? It’s tougher. The 30-year refinance rate is hovering around 6.56%.

👉 See also: Is Stock Market Up or Down: What’s Actually Happening to Your Money Right Now

Basically, if you bought a house back in 2023 when rates were screaming toward 8%, today looks like a miracle. But if you’re comparing this to the "free money" era of 2021, it still feels expensive. It’s all about perspective.

Why Did Rates Just Drop?

It wasn't just the Federal Reserve.

Actually, the Fed has been cutting rates—they've done it three times in their last three meetings—but mortgage rates don't always follow them like a lost puppy. In late 2024, the Fed cut rates and mortgage rates actually went up.

This time, the "Trump Effect" is the culprit. On January 9, a post on Truth Social about directing $200 billion into the mortgage bond market sent yields tumbling. When the government (or its entities) buys more mortgage-backed securities, the increased demand drives prices up and yields—your interest rate—down.

Sam Khater, the chief economist over at Freddie Mac, noted that this has pushed purchase applications up over 20% compared to last year. People are finally coming off the sidelines.

The Spread and the 10-Year Treasury

If you want to sound like an expert at your next dinner party, stop talking about the Fed and start talking about the 10-Year Treasury yield.

Mortgage rates usually track about 2% (the "spread") above the 10-year Treasury. When investors get nervous about the global economy or inflation, they buy Treasuries, yields fall, and your mortgage gets cheaper. Right now, that spread is finally narrowing a bit as the market feels a little more stable than it did a year ago.

What Most People Get Wrong About Today's Rates

A lot of buyers are waiting for 3% or 4%.

I'm going to be real with you: that's probably not happening. Experts like Ted Rossman from Bankrate suggest that while we might see rates dip to 5.5% later in 2026, the days of sub-4% rates were a fluke of a global pandemic.

The "new normal" is likely the 5.5% to 6.5% range.

🔗 Read more: Rite Aid Larchmont Boulevard: The Real Story Behind the Neighborhood’s Most Talked-About Closure

Another misconception? Thinking a lower rate always means a better deal. If rates drop to 5.7% this spring, every single person who has been waiting since 2024 is going to rush the market. You know what that means. Bidding wars. Over-asking prices. Waived inspections.

Sometimes, paying 6.1% in a quiet January is cheaper than paying 5.7% in a frenzied April where you have to bid $50,000 over asking just to get the keys.

The Regional Reality

Rates aren't the same in Florida as they are in Oregon.

Lenders price risk differently based on local markets. If you’re looking at a "Jumbo" loan (for those expensive houses that exceed conforming limits), you’re looking at roughly 6.40% today. VA loans—thank you for your service—are slightly higher at 6.26%, but they usually come with much lower down payment requirements, which balances the scales.

Is It Time to Lock In?

This is the $500,000 question.

If you are under contract right now, you’re in a weird spot. The market is volatile. Mortgage News Daily reported that some lenders were bumping rates back up yesterday morning because the bond market took a slight hit after the initial Trump-fueled rally.

My advice? If the payment works for your budget today, lock it.

Don't gamble your future home on the hope that rates will drop another 0.1% next Tuesday. You can always look for a "float-down" option, which some lenders like Bank of America offer, allowing you to snag a lower rate if the market dips before you close.

Actionable Steps for Borrowers

Stop scrolling and do these three things:

🔗 Read more: 15 soles a dolares: What Most People Get Wrong About Small Currency Exchanges

- Check your credit score immediately. A move from a 680 to a 740 score can save you more on your monthly payment than any Federal Reserve meeting ever will.

- Get a "Loan Estimate" from at least three lenders. Don't just look at the rate; look at the "Points" and "Fees" column. A 5.9% rate with $8,000 in closing points is often a worse deal than a 6.1% rate with zero points.

- Run the numbers for a 15-year fixed. If you can swing the higher monthly payment, the interest savings over the life of the loan are staggering—we're talking hundreds of thousands of dollars.

The bottom line is that while what is mortgage interest rates today matters for your monthly budget, the "perfect" time to buy is usually just when you find the right house and the payment doesn't keep you up at night. The market is finally giving us some breathing room. Use it wisely.