You've probably been staring at those Zillow alerts for months. Maybe years. It feels like every time you get close to pulling the trigger, the numbers shift. Well, it's Wednesday, January 14, 2026, and the vibe in the housing market just changed—big time.

Honestly, the "normal" we used to know is dead. But what's happening right now is actually kind of wild.

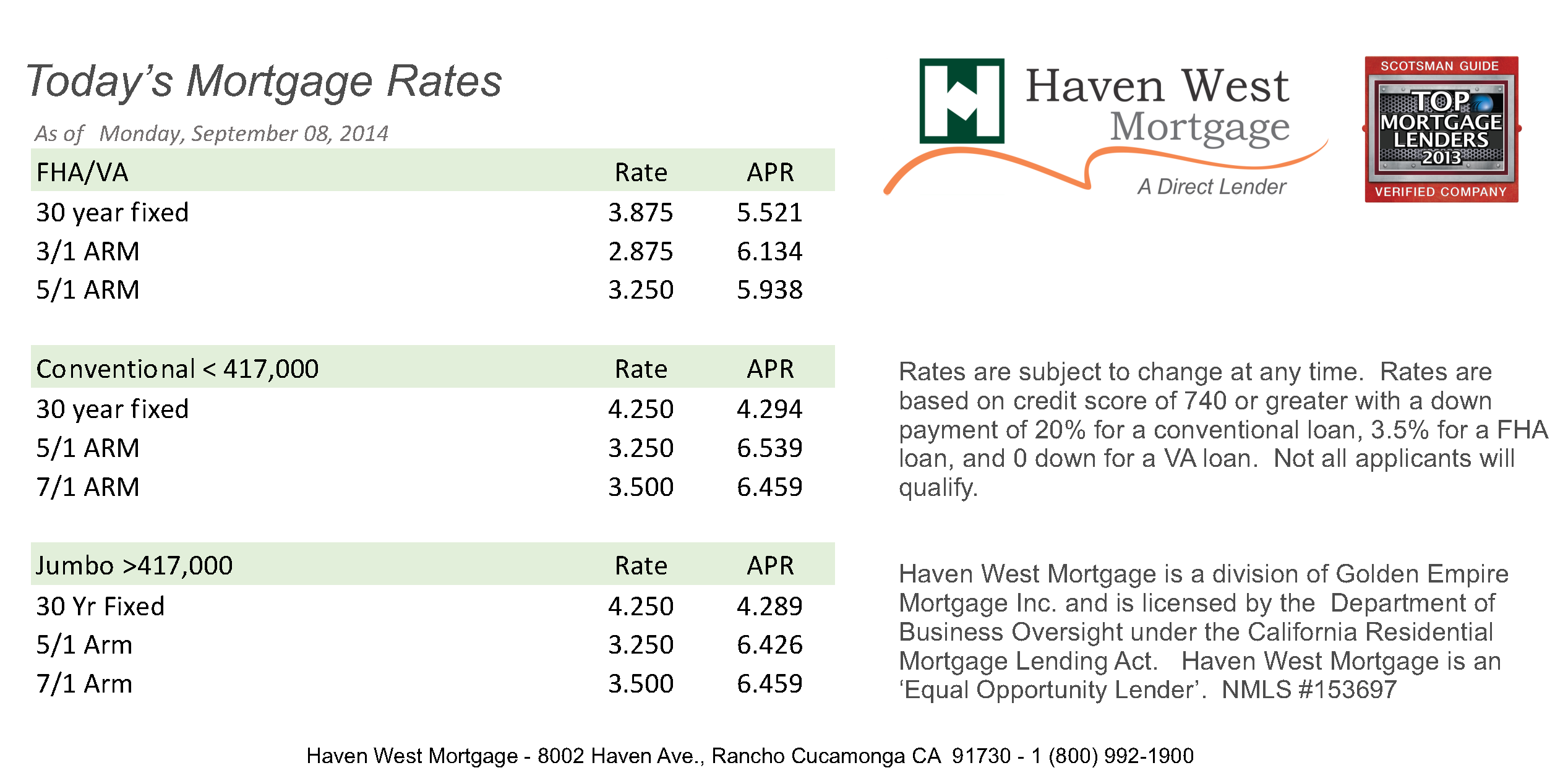

What is mortgage rates today?

If you're looking for the quick answer, here's the deal: the national average for a 30-year fixed mortgage is sitting right around 6.14% today.

But that's just the average. Some lenders are already dipping their toes into the 5.9% range. This is a massive deal because we haven't seen rates stay consistently under that 6% psychological barrier in ages. Just last week, we were looking at 6.25% or higher. It doesn't sound like a lot, but on a $400,000 loan, that tiny move saves you enough every month to cover a decent car payment or a lot of groceries.

Why the sudden dip?

✨ Don't miss: Family Dollar store manager pay: What Most People Get Wrong

It’s mostly coming from the White House and some aggressive new moves by Fannie Mae and Freddie Mac. The government basically stepped in and said they’re going to buy $200 billion in mortgage-backed securities. When they do that, it puts downward pressure on rates. It's like a shot of adrenaline for the housing market.

The breakdown by loan type

- 15-Year Fixed: These are looking even better, averaging around 5.53%. If you can swing the higher monthly payment, you’re saving a fortune in the long run.

- 30-Year FHA: These are hovering near 6.24%.

- Jumbo Loans: If you're buying a mansion (or just a normal house in California), you’re looking at about 6.38%.

- 5/1 ARMs: Ironically, these are actually higher than fixed rates right now, coming in at 5.53% to 6.17% depending on the lender. It’s an "inverted" situation that makes zero sense for most buyers right now.

Why your neighbor got a better rate than you

I’ve seen people get frustrated because they see a 5.8% advertised online but get quoted 6.4%.

It’s not always a scam.

Lenders are getting incredibly picky about credit scores again. If you’re not at a 740 or higher, you’re paying a "risk premium." Also, location matters more than people realize. In New Jersey, rates are averaging closer to 5.87%, while in New York, you might be stuck with 6.25% for the exact same house.

The Trump effect and the 2026 housing "surge"

There is a lot of talk about a "2026 surge" in the housing market.

✨ Don't miss: XRP ETF Filing Amendments: What Most People Get Wrong

The National Association of Realtors is actually predicting a 14% jump in home sales this year. That’s huge. The theory is that millions of people have been "locked in" to their 3% pandemic rates and were too scared to move. But now that rates are drifting toward 5.5% or 5.7%, that gap is finally small enough for people to justify selling.

But here is the catch.

More buyers mean more competition. If everyone who was waiting on the sidelines jumps in at the same time, we might see home prices start climbing again. It's the classic "catch-22" of real estate. You get a lower interest rate, but you end up paying $30,000 more for the house because you're in a bidding war with ten other people.

What the experts are saying

Ted Rossman, a senior analyst at Bankrate, thinks we could see 5.5% by the end of the year if the economy cools down. On the flip side, some folks at the Mortgage Bankers Association are more cautious, thinking we'll stay stuck in the low 6s because inflation is being stubborn.

🔗 Read more: NYL Term Life Insurance: Why This Giant Is Actually Worth the Higher Price Tag

Nobody has a crystal ball.

If inflation reports come back "hot" next month, these 5.9% rates could vanish overnight. The Fed is still playing a very delicate game with interest rates, and they aren't afraid to hike them back up if they think the economy is getting too "toasty."

Should you lock in today?

This is the million-dollar question.

If you're currently sitting on a rate from 2023 or 2024 when things were hitting 7% or 8%, a refinance is starting to look like a brilliant move. Saving $300 a month pays for the closing costs of a refi pretty quickly.

If you’re a buyer, don't wait for 3% again. It’s not happening. Most economists agree that those sub-4% rates were a once-in-a-lifetime fluke caused by a global shutdown. If you find a house you love and the payment at 6% fits your budget, marry the house and "date the rate." You can always refinance later if things drop to 5%, but you can't go back and buy today's inventory.

Actionable steps for right now

- Check your credit score today. Even a 20-point bump could move you from a 6.3% rate to a 5.9% rate. That's thousands of dollars.

- Compare at least three lenders. Don't just go with your primary bank. Check a local credit union and an online lender like Rocket or Better.

- Ask about "buying down" the rate. Sometimes paying a few thousand dollars upfront (points) to get a permanent 5.5% rate makes way more sense than taking the "free" 6.1% rate.

- Watch the 10-Year Treasury yield. Mortgage rates usually follow the 10-year Treasury. If you see that yield dropping on the news, call your loan officer immediately.

The market is moving fast. January 2026 is already proving to be a turning point for anyone who felt priced out of the American Dream over the last few years. Keep your paperwork ready, because when the right house hits the market at these new lower rates, it won't stay there for long.