You’re probably thinking about 65. That’s the magic number, right? Everyone talks about the 65th birthday like it’s this grand gateway to cheap healthcare and government-backed peace of mind. But honestly, the answer to when can I get Medicare is a lot messier than a single candle on a cake.

It depends on your health. It depends on your work history. It even depends on whether you're currently dealing with a specific type of chronic illness that the government deems "eligible." If you wait too long, Uncle Sam hits you with penalties that last—literally—the rest of your life.

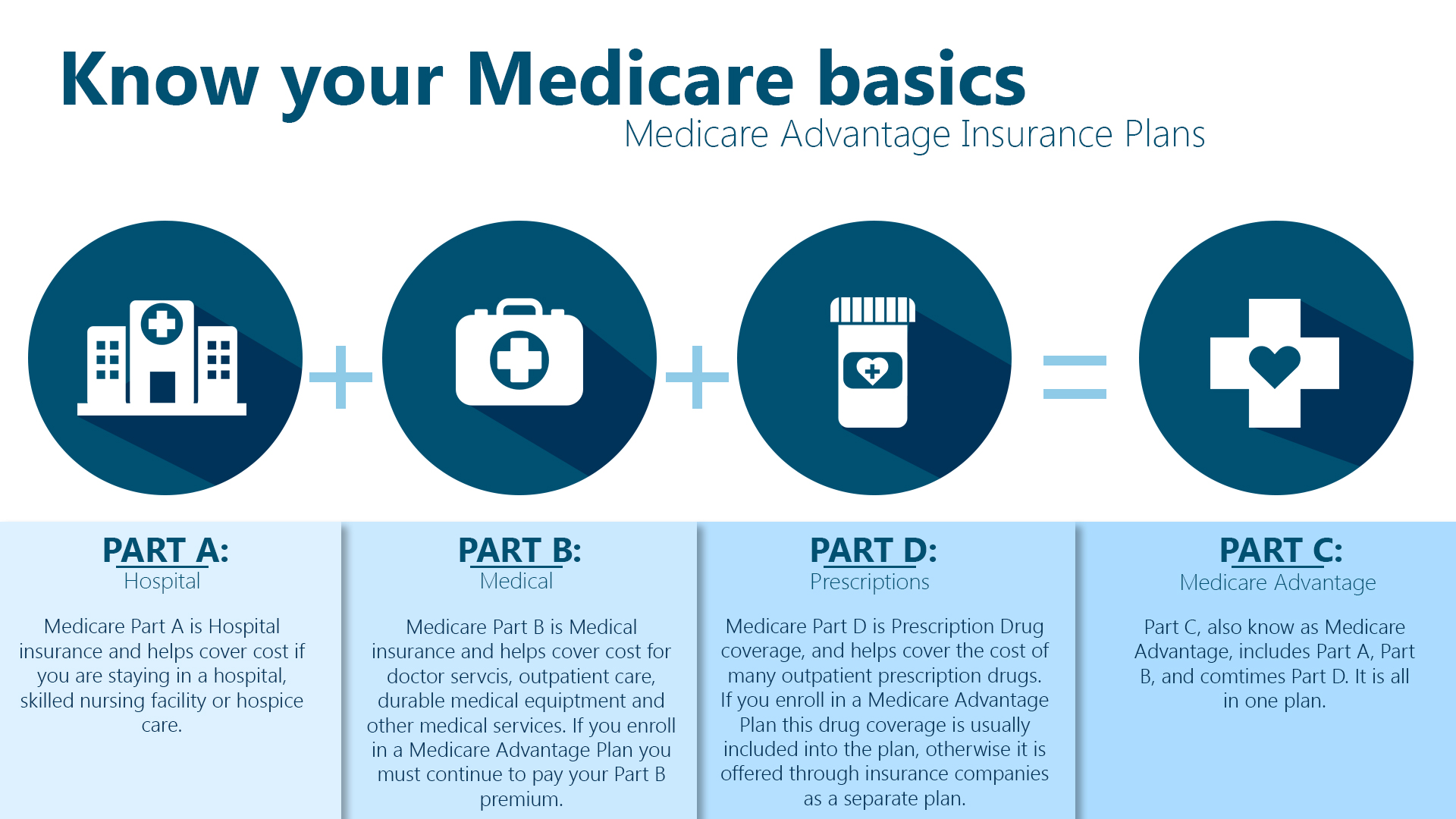

The Standard 65-Year-Old Path

Most people fall into the "Initial Enrollment Period" or IEP. This is a seven-month window. It’s not just your birth month. You get the three months before you turn 65, the month you actually hit the milestone, and then the three months after.

If you’re already collecting Social Security, you don’t even have to lift a finger. The government just sends you the red, white, and blue card in the mail. It shows up about three months before your 65th birthday. You’re "deemed" enrolled in Part A and Part B automatically.

But what if you’re still working? This is where people get burned.

If you have "creditable" coverage from a large employer (usually 20 or more employees), you might not need Part B yet. Part A is usually free anyway if you’ve worked 10 years in the US. But if your company is tiny—under 20 people—Medicare actually becomes your primary payer the moment you turn 65. If you don't sign up, your private insurance can legally refuse to pay your bills, leaving you with a five-figure hospital tab because you thought you were "covered" by your job. It happens more often than you'd think.

When Can I Get Medicare Early?

You don't always have to wait for the gray hair. Disability is the big exception.

If you have been receiving Social Security Disability Insurance (SSDI) checks for 24 months, you automatically get Medicare on the 25th month. You don't have to be 65. You could be 25. The math is simple: 24 months of checks equals Medicare eligibility.

There are two major shortcuts to this rule where the 24-month waiting period is waived entirely:

- ALS (Amyotrophic Lateral Sclerosis): If you are diagnosed with Lou Gehrig’s disease, you get Medicare the very first month your disability benefits start. No waiting.

- End-Stage Renal Disease (ESRD): This is permanent kidney failure requiring dialysis or a transplant. Usually, coverage starts on the first day of the fourth month of your dialysis treatments.

The Trap of the Special Enrollment Period

Life doesn't always happen in seven-month windows. Maybe you retired at 67. Maybe your spouse lost their job and you were on their plan.

👉 See also: Vitamin From Sun: Why You’re Probably Not Getting Enough (And What to Do)

When you lose that employer coverage, you trigger a Special Enrollment Period (SEP). You have eight months to sign up for Part B without a penalty. If you miss that eight-month window because you were "figuring things out" or traveling, you are stuck. You have to wait for the General Enrollment Period, which only runs from January 1 to March 31 each year.

And here is the kicker: for every 12-month period you could have had Part B but didn't, your premium goes up 10% for life. That is a permanent tax on your retirement for a simple paperwork mistake.

Part D and the "Hidden" Deadline

Most people obsess over Part A (hospitals) and Part B (doctors). They forget Part D (drugs).

Even if you don't take a single pill today, the government expects you to have "creditable" prescription drug coverage. If you go 63 days or more without it after you turn 65, they start tacking on a 1% penalty per month for every month you were uncovered. You’ll pay that extra amount as long as you have a Medicare drug plan.

Navigating the Weird Nuances

What if you're a veteran? VA benefits are great, but they aren't the same as Medicare. Many vets keep both because the VA can sometimes be slow or limited in which doctors you can see.

What if you have an HSA (Health Savings Account)? Stop contributing to it at least six months before you apply for Medicare. If you don't, you'll face a tax penalty from the IRS because you cannot legally contribute to an HSA once you are on Medicare. It’s a bizarre interaction between the tax code and healthcare law that catches thousands of people off guard every year.

Practical Steps to Take Right Now

- Check your Social Security status. Go to ssa.gov and create an account. See if you’re already set for automatic enrollment or if you need to file an application.

- Audit your current employer plan. If you’re over 65 or nearing it, ask your HR department specifically: "Is this coverage primary or secondary to Medicare?" Get it in writing.

- Mark the 'Three Months Prior' date. If you aren't on Social Security, you need to manually apply three months before your 65th birthday month to ensure your coverage starts on day one.

- Verify 'Creditable Coverage'. If you are staying on a private plan, ensure you receive a "Notice of Creditable Coverage" every year. This is your "Get Out of Jail Free" card to avoid late enrollment penalties later.

- Evaluate your drug costs. Use the Medicare.gov Plan Finder tool to see if a $0 or low-premium Part D plan is worth it just to "park" your eligibility and avoid future penalties.

The system isn't designed to be intuitive. It's designed to be a bureaucratic machine. Knowing when can I get Medicare is less about the date on your birth certificate and more about understanding which window is currently open for your specific life situation.