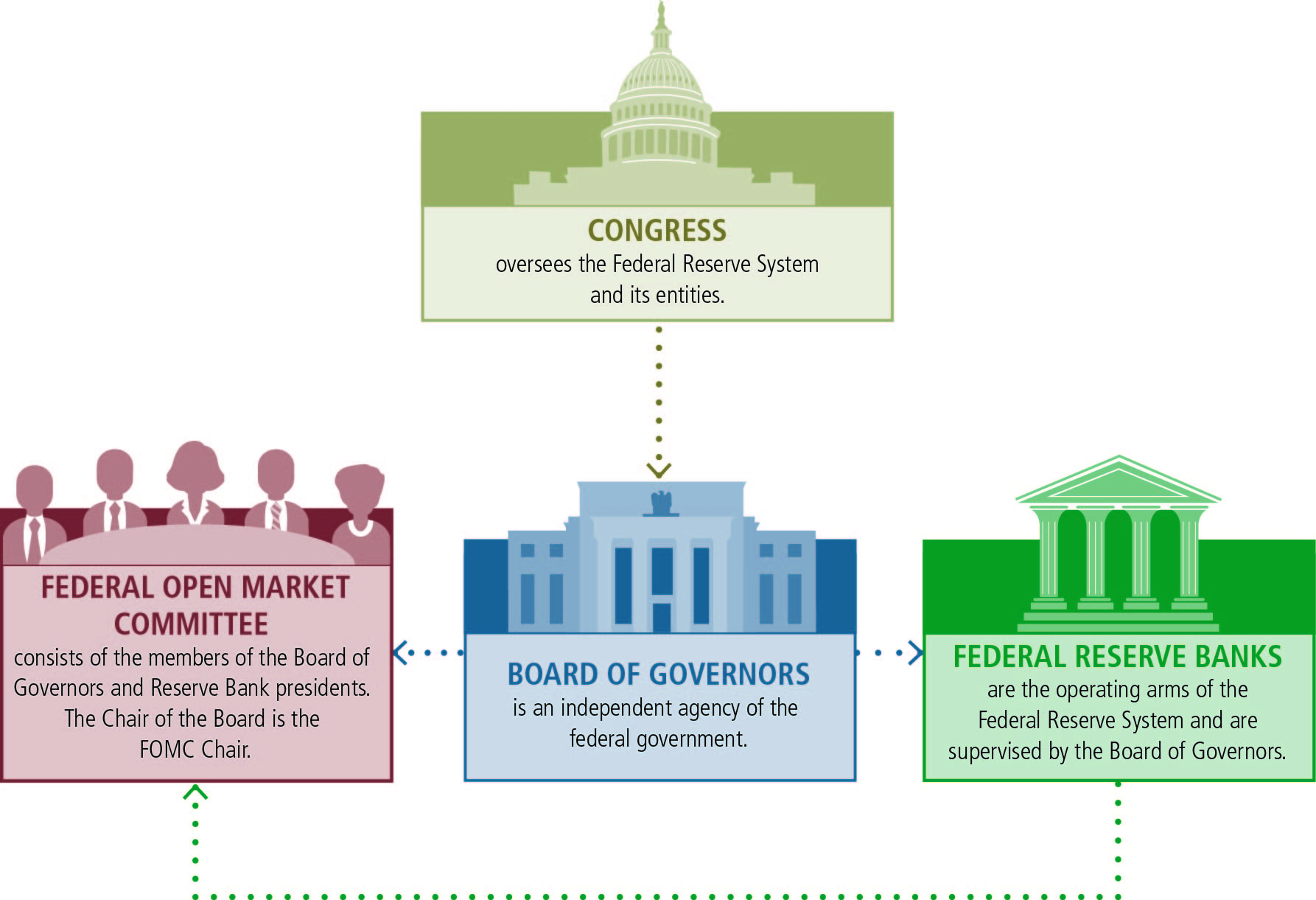

If you’re watching your mortgage rate or wondering why your savings account yield just hit a plateau, you’ve probably been keeping a nervous eye on the Eccles Building in D.C. Honestly, the drama surrounding the central bank has reached a fever pitch lately. Between the "will-they-won't-they" interest rate dance and the unprecedented political friction between the White House and Chairman Jerome Powell, everyone is asking the same thing: when does federal reserve meet next?

The short answer is soon. Specifically, the Federal Open Market Committee (FOMC) is scheduled to wrap up its first major meeting of the year on January 28, 2026.

👉 See also: Australian USD to PKR: What Most People Get Wrong About This Currency Math

But just knowing the date isn't enough anymore. Not in this economy. We are currently in a bizarre "blackout period" where Fed officials aren't allowed to speak publicly, leaving the rest of us to guess what they’re thinking behind closed doors. With the effective federal funds rate sitting at 3.64%, the stakes for this January meeting are massive.

When Does Federal Reserve Meet Next: The 2026 Calendar

The Fed doesn't just wake up and decide to change the world’s economy on a whim. They have a very rigid, eight-meeting schedule. If you’re trying to plan a big purchase or time a market entry, these are the dates you need to circle in red on your kitchen calendar.

- January 27-28 (The big one coming up)

- March 17-18 (Includes updated economic projections)

- April 28-29

- June 16-17 (Includes updated economic projections)

- July 28-29

- September 15-16 (Includes updated economic projections)

- October 27-28

- December 8-9 (The final meeting of the year)

Most people assume every meeting is the same, but that’s a total myth. The meetings in March, June, September, and December are the "heavy hitters" because that’s when the Fed releases its Summary of Economic Projections (SEP) and the infamous "Dot Plot."

The Dot Plot is basically a scatter chart where anonymous Fed members guess where rates will be in the future. It’s not a promise, but it’s the closest thing we have to a crystal ball.

What’s actually happening on January 28?

So, the January 28 meeting is a two-day affair. On Tuesday, they talk shop. On Wednesday, they release the statement at 2:00 PM ET, followed by Jerome Powell’s press conference at 2:30 PM.

If you want to see the market go crazy in real-time, just watch the S&P 500 chart at 2:31 PM.

The Politics and the Pressure: Why 2026 is Different

Usually, the Fed is as boring as a tax audit. Not this year.

Chairman Powell is currently navigating a minefield. His term as Chair actually ends in May 2026, and President Trump has made no secret of the fact that he wants someone more "flexible" (read: someone who will cut rates faster) in that seat. Names like Kevin Hassett and Kevin Warsh are already floating around as potential replacements.

The drama took a dark turn just a few days ago. On January 11, Powell revealed that the Department of Justice served the Fed with subpoenas regarding testimony he gave last June. It’s unprecedented. While the DOJ claims it’s about a building renovation project, many insiders—including Powell himself—hint that it’s a hardball tactic to force his hand on interest rates.

Despite the "intimidation," the Fed is trying to stay independent. Central bankers from around the world even signed a letter of solidarity last week to support Powell. It’s a mess, frankly. But for you, it means the January meeting might be more about proving independence than actually moving the needle on rates.

Why a Rate Cut in January is Looking Unlikely

A few months ago, everyone was betting on a cut in January. Now? Not so much.

💡 You might also like: 3000 usd in gbp: How Much You Actually Get After the Fees

The CME FedWatch tool, which tracks what traders are actually betting their money on, shows only a 5% chance of a rate cut this month. That’s a huge drop from the 24% chance we saw just thirty days ago.

Why the change of heart?

- Inflation is "Sticky": December’s CPI came in at 2.7%. The Fed’s target is 2.0%. While we’ve come a long way from the 9% highs of 2022, that last little bit of inflation is proving hard to kill.

- The Labor Market is Weirdly Strong: Unemployment actually dropped to 4.4% in December. Usually, you cut rates to save jobs. If the job market is fine, the Fed feels they can keep rates higher to keep fighting inflation.

- Tariff Fears: The "reciprocal tariffs" enacted last August are starting to filter through to shelf prices. Powell warned in December that goods inflation is picking up specifically in sectors hit by tariffs. He calls it a "one-time shift," but the Fed doesn't want that shift to turn into a permanent upward spiral.

Real-World Impact: What This Means for Your Wallet

When you ask when does federal reserve meet next, what you’re really asking is "when is my life going to get cheaper?"

If the Fed holds rates steady at 3.50%–3.75% (the current range) during the January 28 meeting, don't expect your credit card interest to drop. Bank prime loans are sitting around 6.75% right now. That’s expensive.

However, if you are a saver, this is kind of a golden era. High-yield savings accounts (HYSAs) are still offering rates that actually beat inflation for the first time in a decade. If they "pause" in January, those yields stay high for a bit longer.

On the flip side, the "hawks" on the committee—the people who want to keep rates high to crush inflation—are gaining more power. Several vocal hawks just rotated into voting spots for 2026. This means even if Powell wants to cut, he might not have the votes to do it.

Actionable Steps for the January Meeting

Don't just sit there and watch the news crawl. Here is how you should handle the lead-up to the January 28 decision:

- Lock in your HYSA now: If the Fed does surprise everyone with a cut, bank yields will drop fast. Lock in a high-yield account or a CD while the federal funds rate is still at 3.64%.

- Watch the 2:30 PM Presser: Listen for the word "neutral." Powell mentioned in December that rates are finally within a "range of plausible estimates of neutral." If he says they are above neutral, a cut is coming in March. If he says they have "work to do," expect high rates through the summer.

- Ignore the political noise: The subpoenas and the White House tweets make for great headlines, but the Fed historically sticks to the data. Watch the PCE (Personal Consumption Expenditures) reports instead of the news.

The January meeting is likely to be a "wait and see" event. With the government shutdown last fall disrupting some economic data, the committee is flying a bit blind. They’ll likely keep the status quo, watch the tariff impact in Q1, and wait until the March 17-18 meeting to make a move. Keep your eye on the data, not the drama.