The Old Guard is Getting a Face-Lift

Whole life insurance. It usually sounds about as exciting as watching paint dry or reading the fine print on a toaster warranty. For years, the narrative was simple: "Buy term and invest the difference." It was the mantra of every financial guru with a radio show. But honestly, the world has shifted. In 2026, the conversation around whole life insurance has moved past the "is it a scam?" Reddit threads and into a space where it's actually being used as a tactical tool for a very weird economy.

Interest rates are finally doing something interesting. After a decade of being stuck in the basement, they’ve stayed "higher for longer," and that is trickling down to policyholders in a way we haven't seen since the early 2000s.

It’s not just about the death benefit anymore. It’s about the "living benefits"—a term the industry loves to throw around, which basically means you don't have to die to see the value. People are looking at these policies as a way to hedge against market volatility that feels more like a roller coaster than a retirement plan.

The Dividend Comeback: Real Numbers for 2026

If you’ve been following the big mutual companies—the heavy hitters like Northwestern Mutual, MassMutual, and Guardian—you’ve probably noticed something. They are bragging. And for once, they actually have something to brag about.

✨ Don't miss: Dollar to New Zealand Dollar: Why the Exchange Rate is Acting So Weird Right Now

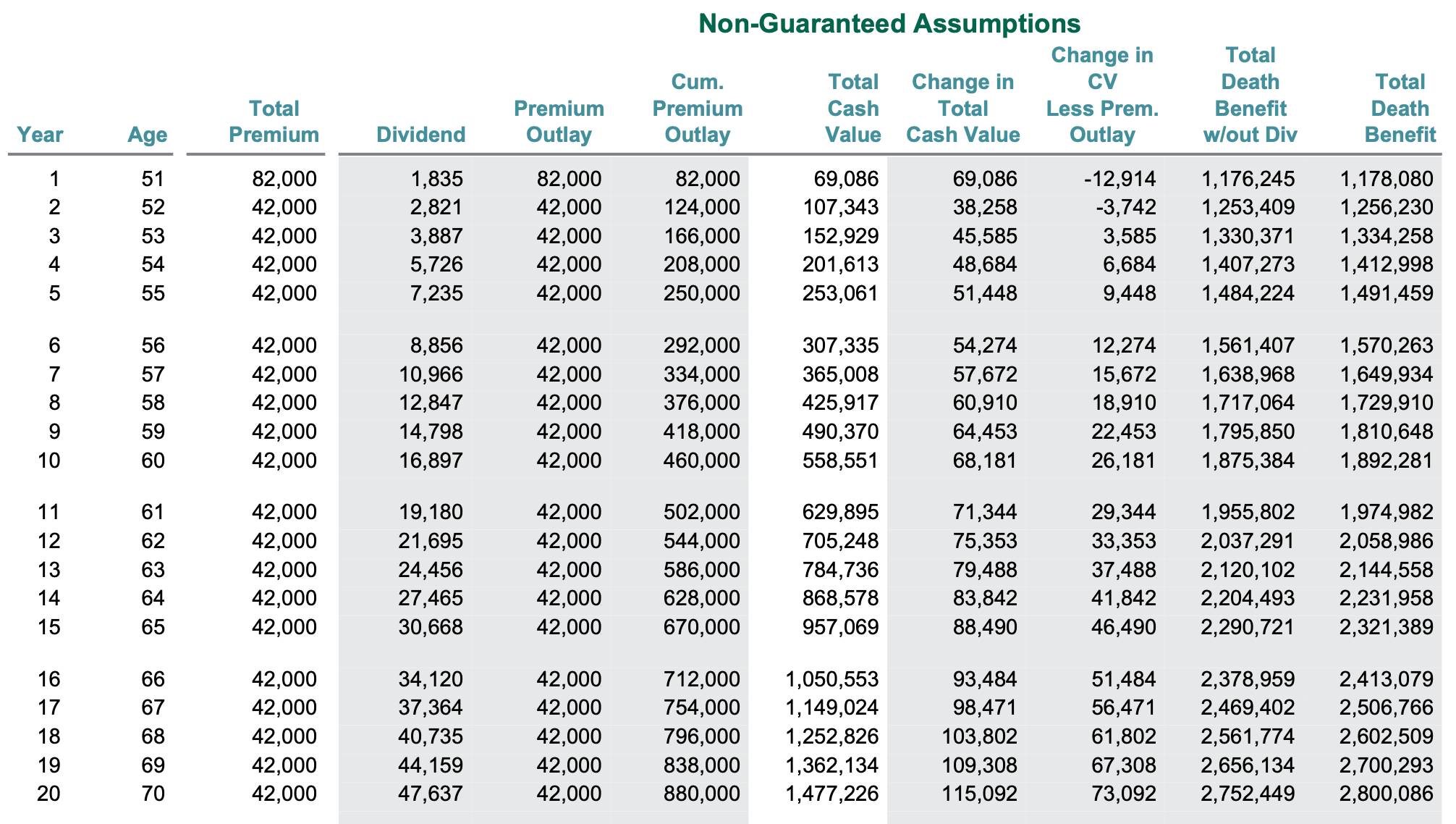

Northwestern Mutual recently announced a record-breaking $9.2 billion dividend payout for 2026. That’s not a typo. It’s nearly a billion more than their 2025 award. MassMutual and New York Life are following suit, with dividend crediting rates trending upward toward the 6.25% to 6.60% range.

Important Distinction: A 6.60% dividend crediting rate is NOT the same as a 6.60% return on your money.

The insurance company takes their cut for expenses and mortality charges before that rate touches your cash value. It's a bit of a shell game, but the trend is undeniably positive. For a long time, these dividends were slowly sinking. Now? They’re the "cool kid" of the conservative investment world again.

Why the Under-40 Crowd is Suddenly Interested

You wouldn't think 30-year-olds would care about permanent life insurance. They're usually worried about rent or whether they can afford a house that isn't a fixer-upper in the middle of nowhere. But Capgemini’s World Life Insurance Report 2026 points to a massive shift.

Younger generations are starting to see whole life insurance as a "portable" financial foundation. In an era where "job-hopping" is just called "having a career," group life insurance through an employer feels like a trap. You leave the job, you lose the coverage. A private whole life policy stays with you.

Living Benefits are the Hook

Millennials and Gen Z are obsessed with "use-case" value. They want to know: "What can this do for me while I'm alive?"

- Chronic Illness Riders: The ability to tap into the death benefit if you get a nasty diagnosis.

- Cash Value for Major Milestones: Using the policy as a "bank" for a down payment or starting a business.

- Tax-Deferred Growth: In 2026, with talk of tax brackets shifting, the "tax-free" nature of policy loans is a huge selling point.

The Death of the Medical Exam (Sorta)

Remember the days when getting insurance meant a stranger coming to your house to poke you with a needle and ask for a urine sample? Yeah, that's becoming a relic.

Insurtech is the reason. Companies like Ethos and new products like SBLI’s OmniTrak are using "fluidless underwriting." They look at your prescription history, your motor vehicle record, and even data from your wearable tech (if you let them).

About 60% of applicants in 2026 are getting approved without a medical exam. It's fast. It's convenient. But—and there's always a "but"—it’s usually more expensive. If you’re a marathon runner with perfect blood pressure, you might actually want the needle. It could save you 15% on your premiums because you're proving you aren't a risk.

Misconceptions That Just Won’t Die

We need to be real for a second. Whole life is not a get-rich-quick scheme.

If you buy a policy today, your cash value in Year 2 is going to look depressing. It might even be zero. Most of your early premiums go toward the agent's commission and the company's overhead. It takes roughly 10 to 15 years for a policy to "break even"—where the cash value equals what you've paid in.

📖 Related: WMT Check-in: What's the price of walmart stock today and why it's moving

Also, "Infinite Banking" is a term you'll see all over TikTok. It sounds magical. "Be your own bank!" they say. Basically, you're just borrowing your own money and paying interest back to the insurance company. It can work, but it requires a level of discipline most people honestly don't have. If you don't pay back the loan, your death benefit shrinks, and if the policy lapses with a big loan, you could face a massive tax bill.

The 2026 Landscape: What to Look For

If you’re shopping for whole life insurance this year, the market is different than it was even 24 months ago. Here is what's actually happening on the ground:

- Hybrid Products: We’re seeing more "modular" policies. You can start with a base whole life policy and "bolt on" term riders or long-term care riders as your income grows.

- Climate-Linked Incentives: Some forward-thinking carriers are starting to offer "wellness" discounts that include environmental factors or lifestyle choices that reduce stress—kinda weird, but it's happening.

- AI-Driven Customization: Instead of "Standard" or "Preferred" ratings, AI is allowing for "micro-rating." You might get a slightly better rate because you live in a specific zip code or have a specific combination of healthy habits.

Actionable Steps: Is This for You?

Don't just take an agent's word for it. They're making a commission, after all.

First, check your "Duration" fit. If you don't plan on keeping this policy for at least 20 years, don't buy it. You'll lose money. Whole life is a marathon, not a sprint.

✨ Don't miss: Rite Aid Spokane Shadle Explained: What You Need to Know Now

Second, ask for the "Internal Rate of Return" (IRR) illustration. Don't just look at the big numbers in the "Assumed" column. Look at the "Guaranteed" column. That is the worst-case scenario. If you can't live with the guaranteed numbers, the policy isn't for you.

Third, diversify your "Tax Buckets." Most people have a 401(k) (tax-deferred) and maybe a brokerage account (taxable). Whole life fits into the "tax-advantaged" bucket. It shouldn't be your only investment. It should be the "boring" part of your portfolio that provides a floor when the stock market decides to tank.

Finally, look at the company's Comdex score. It’s a composite ranking of all the major rating agencies (A.M. Best, Moody’s, S&P). You want a company with a score of 90 or higher. In a world of 2026 uncertainty, you want a carrier that’s been around since the Civil War and plans to be around for another century.

The reality of whole life insurance today is that it's no longer a "one size fits all" product. It's a complex, high-maintenance financial tool that, when used correctly, offers a level of certainty that's becoming increasingly rare. Just make sure you know exactly what you're signing up for before you write that first check.