Math isn't always about rocket science. Sometimes, it’s about the small stuff. You’re likely here because you need a quick answer, or maybe you're staring at a bill, a tax form, or a tip jar and trying to figure out if you're being ripped off.

It’s $0.66.

That’s the number. Simple. But why does such a tiny decimal matter? In the world of finance, retail, and even local government budgeting, 3 percent of 22 acts as a fundamental building block for much larger calculations.

Most people don't think about 66 cents. They shouldn't. But when you scale that up to millions of transactions or use it as a basis for a interest rate hike, it starts to carry some serious weight. Let's look at how we get there and why your brain might be overcomplicating a calculation that a fifth-grader could do on their fingers.

Breaking Down the Math: No Calculus Required

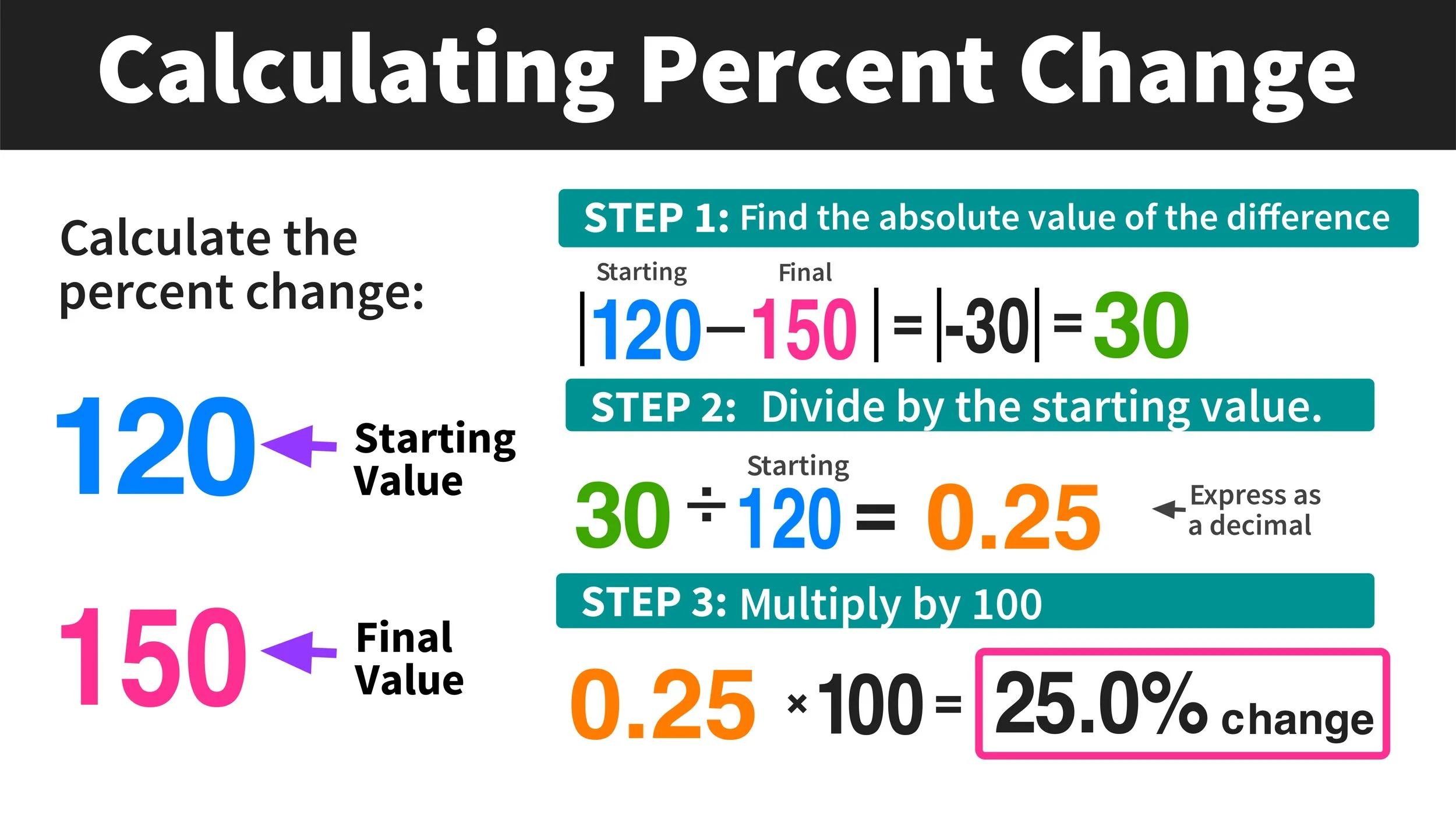

Calculating 3 percent of 22 is straightforward if you remember the "of" rule. In math, "of" basically always means multiply.

You take the percentage, turn it into a decimal (0.03), and hit it against your whole number.

$$0.03 \times 22 = 0.66$$

If you’re doing this in your head while standing in a checkout line, there's a "mental math" hack that makes you look like a genius. Find 1% first. Move the decimal two places to the left on 22, and you get 0.22. Now, just triple it.

0.22 plus 0.22 plus 0.22.

Boom. $0.66$.

It's actually kind of satisfying when the numbers are this clean. No trailing decimals, no infinite repeating 9s. Just a solid, two-digit result that fits neatly into a coin purse.

Where This Number Actually Shows Up

You’d be surprised how often this specific ratio pops up in the real world.

Take credit card processing fees. If you own a small coffee shop and a customer buys a $22 bag of artisanal beans, you aren't seeing all that money. Most merchant services charge somewhere around 3%. When that transaction clears, the bank is taking their 3 percent of 22, leaving you with a smaller margin than you thought.

It’s the "hidden tax" of the digital economy.

Then there’s the world of sports and statistics. Imagine a baseball player who has 22 plate appearances in a very short stint or a specific situational window. If they have a 3% walk rate—which is admittedly terrible for the MLB, where the average is closer to 8% or 9%—they’ve basically walked less than one time. They are effectively at a fraction of a successful outcome.

In real estate, 3% is a common commission for a single side of a transaction. If you're looking at a micro-lease or a tiny monthly storage rental of $22, that 66 cents is what's going to the agent. It seems like nothing until you realize these micro-transactions happen by the thousands every single day in urban centers like New York or London.

The Psychology of the "Small Percent"

Humans are notoriously bad at estimating small percentages of small numbers. We tend to round down to zero.

💡 You might also like: Why 1 USD in JMD is Always Changing and What It Means for Your Pocket

Behavioral economists like Daniel Kahneman, who wrote Thinking, Fast and Slow, often discussed how we use heuristics—mental shortcuts—to make decisions. When we see a 3% increase on a $22 item, our brain tells us "that’s basically free."

But inflation is a sneaky beast.

If every $22 item in your grocery basket goes up by 3%, and you buy 50 of those items a year, you’re looking at a cumulative drain on your wallet that most people fail to budget for. It’s the "latte factor" but for math nerds.

We also see this in "junk fees." Ever notice a "Service Fee" or a "Wellness Charge" on a restaurant bill that’s exactly 3%? If your meal was $22, they are tacking on 66 cents. It's small enough that you won't complain to the manager, but large enough to cover the restaurant's rising insurance costs when spread across every table in the house.

Calculating it on Different Devices

Honestly, you probably have a calculator within arm's reach. But every OS handles it differently.

On an iPhone, you type 22, then *, then 3, then the % sign, then =.

On Google Search, you can literally just type "3% of 22" into the search bar, and the built-in widget will give you the answer before you even hit enter.

If you're using Excel or Google Sheets, the formula is even simpler. Just type =22*0.03 into any cell.

Professional accountants often use the "Fraction Method" for this. They know that 3% is just 3/100.

So, $(22 \times 3) / 100$.

66 / 100.

0.66.

It’s the same result, but thinking in fractions helps when you’re dealing with much larger, more complex spreadsheets where percentages aren't whole numbers.

Real-World Context: Is 3% High or Low?

Context is everything.

✨ Don't miss: Status of GA State Refund: Why You Haven't Received It and What to Do

If you’re talking about a 3% yield on a $22 dividend stock, that’s actually pretty decent for a conservative investment. You’re getting 66 cents per share just for holding the stock. If you own 1,000 shares, that’s $660 in passive income.

Conversely, if you’re looking at a 3% interest rate on a loan, that’s historically very low. But if it’s a 3% daily interest rate (which some predatory payday lenders use), you’re in deep trouble.

Even though 3 percent of 22 is always 0.66, the value of that 0.66 depends entirely on whether you are the one paying it or the one receiving it.

Why Precision Matters

In medical dosing or chemical engineering, "rounding off" 0.66 to 0.7 or down to 0.6 can be catastrophic.

If a researcher is mixing a solution and needs a 3% concentration of a reagent in a 22ml sample, they need exactly 0.66ml. Being off by even a tenth of a milliliter could ruin a clinical trial or a laboratory test.

We see this in high-frequency trading as well. Algorithms are programmed to hunt for discrepancies much smaller than 3%. In those environments, the difference between 0.66 and 0.661 is worth millions of dollars over the course of a trading day.

How to Apply This Knowledge

Now that you have the answer, what do you do with it?

If you're looking at this for a tip, please don't tip 3%. The standard in the US is 15-20%. A 3% tip on a $22 meal is 66 cents, which is—frankly—an insult to your server unless the service was non-existent.

If you're looking at this for a discount, a 3% off coupon on a $22 item saves you 66 cents. Is it worth driving across town to use that coupon? Probably not. You’ll spend more than that in gas just getting to the store.

🔗 Read more: Dell Computers Ticker Symbol: Why Everyone is Watching DELL Right Now

However, if you are a business owner, look at your "leakage."

Are you losing 3% of your $22 units to theft, damage, or "spoilage"? That 66 cents per unit adds up. If you sell 10,000 units, you’re losing $6,600. That’s a salary bonus or a new piece of equipment.

Actionable Next Steps:

- Audit your small subscriptions. Check your bank statement for any recurring $22 charges. Are they creeping up by 3% or more each year? Companies love the "slow boil" price increase.

- Practice the "1% Rule." Next time you need to find a percentage, find 1% first by moving the decimal. It makes you faster at analyzing deals on the fly.

- Check the fine print. If you see a "3% surcharge" on a contract or bill, calculate the dollar amount immediately. Don't let the smallness of the percentage trick you into ignoring the actual cost.

- Use decimals for accuracy. When working in spreadsheets, always use 0.03 rather than the percent format if you're experiencing rounding errors in your final totals.