You’ve seen the headlines. The numbers coming out of Hsinchu are, frankly, mind-boggling. We’re talking about a company that basically owns the brain of every AI model on the planet. Yet, if you look at your brokerage app lately, the ticker for Taiwan Semiconductor Manufacturing Co. (TSM) might be flashing a color you don't like: red.

It feels like a glitch in the matrix. How can a company reporting record-breaking profits and hiking its capital expenditure to a staggering $52 billion or $56 billion for 2026 be seeing its stock price wobble?

The truth is, the market isn't always a direct reflection of a company’s health. Sometimes it’s a reflection of our own collective anxiety. If you’re wondering why TSM stock is dropping right now, you have to look past the "Buy" ratings and into the messy reality of global trade, interest rates, and the sheer weight of expectations.

The "Good News is Bad News" Paradox

On January 15, 2026, TSMC dropped their Q4 2025 earnings. It was a blowout. Revenue hit $33.7 billion, and they beat earnings expectations by a mile, pulling in $3.14 per ADR. They even told us that 2026 revenue would grow by "close to 30%."

So, why the dip?

Wall Street is a "what have you done for me lately" kind of place. But more than that, it’s a "what will you do for me tomorrow" place. When a company like TSMC guides for massive capital spending—we’re talking about a 32% jump in CapEx over last year—it scares some investors.

They see the $54 billion price tag and think about one thing: margins.

Building 2nm fabs and expanding into Arizona, Japan, and Germany is incredibly expensive. TSMC’s management admitted that these overseas operations could dilute gross margins by 2% to 4% over the next few years. For a stock that was priced for perfection, even a tiny "dilution" feels like a punch in the gut.

The Macro Shadow: Tariffs and The Fed

You can’t talk about why TSM stock is dropping without talking about the 800-pound gorilla in the room: geopolitics.

🔗 Read more: Finding the Right Auto Property for Lease Without Getting Ripped Off

Just this month, the market has been rattled by talk of new 25% tariffs on high-end chips like the Nvidia H200 and AMD MI325X. Since TSMC makes almost 100% of those chips, any friction in how they move across borders makes investors twitchy.

Then there’s the Fed.

Treasury yields just hit a four-month high of 4.23%. When yields go up, high-growth tech stocks—even the ones that actually make money like TSMC—often go down. It’s basic math. If you can get a decent return on a safe "risk-free" bond, you're less likely to gamble on a semiconductor giant sitting in a geopolitical hotspot.

Is the AI "Giga Cycle" Exhausting Itself?

There’s a growing debate about whether we’re in an AI bubble or a "Giga Cycle."

TSMC’s CEO C.C. Wei is firmly in the "this is real" camp. He’s mentioned that demand for advanced nodes is currently outstripping supply by about three times. But some analysts, like those at Future Horizons, are whispering about a potential downturn in 2026 if the broader smartphone and automotive markets don't pick up the slack.

👉 See also: How Much in 1 Billion Dollars? The Mind-Bending Reality of Eleven Figures

While AI accelerators are flying off the shelves, the chips inside your next phone or car aren't seeing that same "insatiable" demand. If AI spending takes even a tiny breather while the rest of the industry is sluggish, TSMC gets caught in the middle.

Valuation: The Reality Check

Honestly, TSM had a monster run in 2025. It returned over 55%.

When a stock moves that fast, it often gets ahead of its "intrinsic value." Some discounted cash flow (DCF) models, like those seen on Simply Wall St, have suggested the stock might be overvalued by as much as 50% based on long-term projections.

A lot of the current "drop" is just a healthy rotation. Institutional investors are taking profits from their winners—the big tech names—and moving that money into small-cap stocks or "real asset" industries that haven't surged yet.

It’s not that people stopped believing in TSMC. It’s just that they’re rebalancing their portfolios for a 2026 that looks very different from 2025.

What Actually Matters for Your Portfolio

If you're holding TSM, or thinking about buying the dip, you need to ignore the daily noise and focus on three things:

- Utilization Rates: Watch if those new fabs in Arizona and Taiwan stay full. High CapEx only pays off if the machines are running 24/7.

- The 2nm Ramp: TSMC is moving into volume production of 2nm chips this year. This is where the big margins live. If they pull this off without a hitch, the "margin dilution" fears will likely evaporate.

- Trade Policy: Keep a close eye on the "One Big Beautiful Bill Act" and any specific chip tariffs. These are the "black swan" events that could actually change the long-term thesis.

The current volatility is a classic case of the market trying to digest a lot of complex information at once. TSMC is still the king of the foundry world, but even kings have to deal with high interest rates and trade wars.

Actionable Insights for Investors:

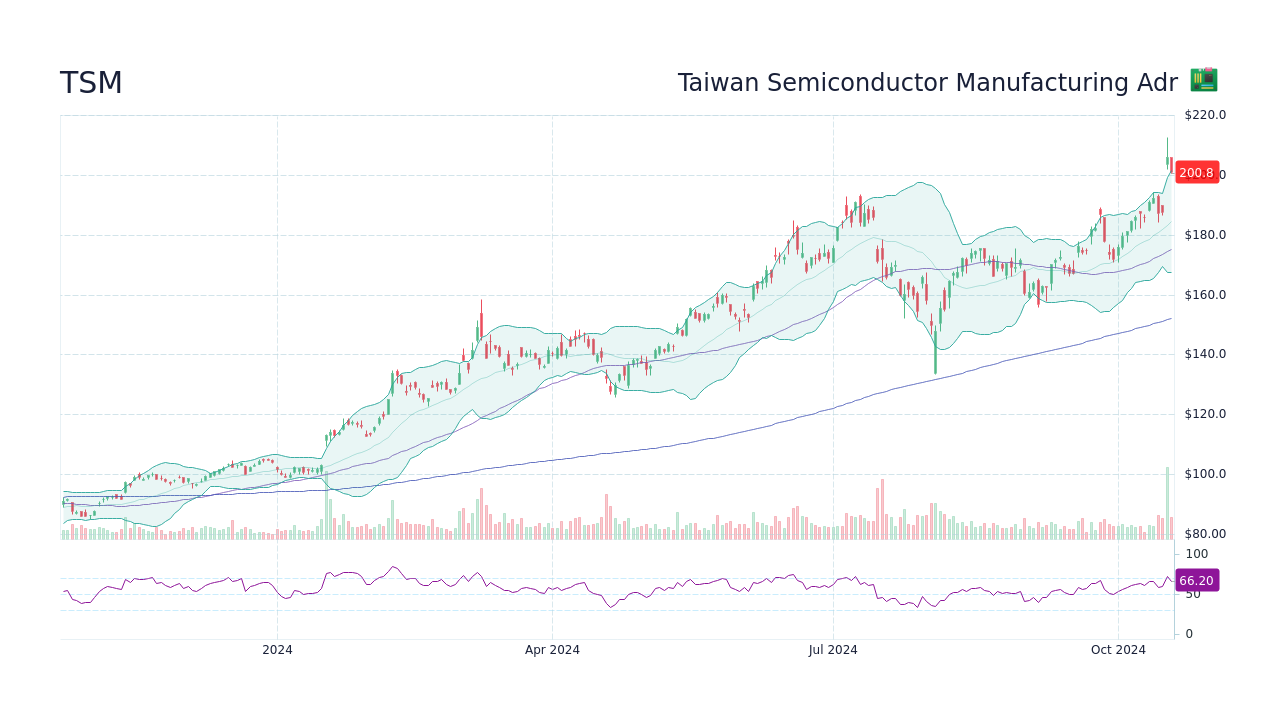

If you're looking at the charts and feeling uneasy, consider tightening your stop-losses or looking at the $282 support level. Many technical analysts see this as a key pivot point; staying above it suggests the long-term uptrend is still intact. Conversely, if you're a long-term believer, focus on the 25% compound annual growth rate (CAGR) the company is targeting through 2029. Short-term price action is often just a distraction from long-term compounding.