Tax season usually feels like a looming cloud, doesn't it? You know it's coming. You know it’s going to cost you something—either time, money, or a significant amount of sanity. Most people start hunting for a 2024 tax brackets calculator the second they get that first W-2 in the mail, hoping for a quick answer. But honestly, most of those digital tools give you a "close enough" number that might actually be way off once the IRS gets involved.

Inflation changed things this year. Big time. Because the cost of living spiked so aggressively over the last couple of years, the IRS made some of the most significant adjustments we've seen in decades to the income thresholds. They do this to prevent "bracket creep," which is basically a fancy way of saying they don't want you to owe more taxes just because you got a cost-of-living raise that didn't actually make you any richer.

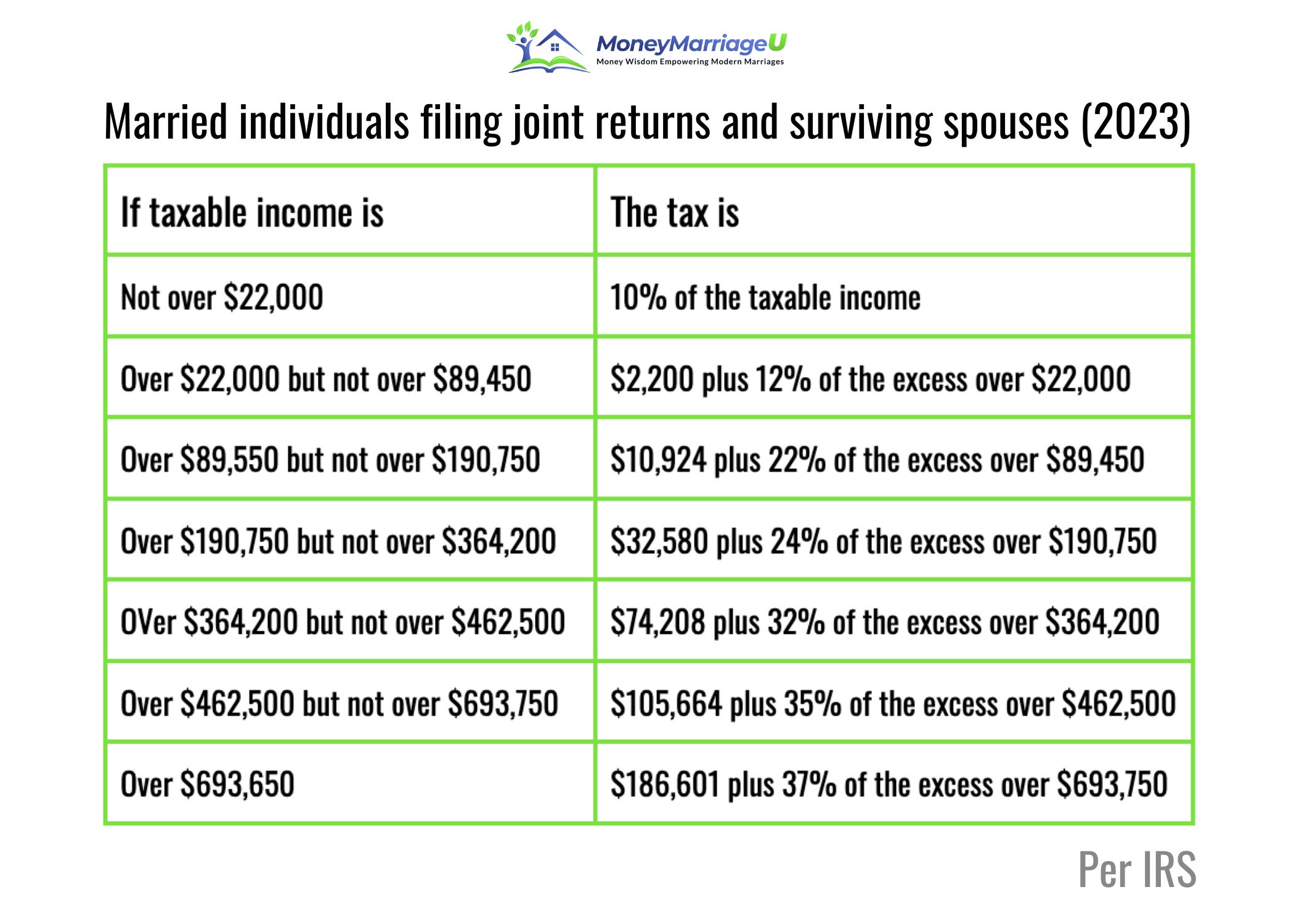

If you're looking at your 2023 returns and assuming 2024 will look the same, you’re probably wrong.

🔗 Read more: Selling Porn Online: What Most People Get Wrong About the Business

How the 2024 Tax Brackets Calculator Changes Your Math

The IRS didn't change the percentages. Those are still stuck at 10%, 12%, 22%, 24%, 32%, 35%, and 37%. What changed is the "bucket" size. For the 2024 tax year (the taxes you are filing right now in early 2025), the income ranges shifted upward by about 5.4%.

Let’s look at a single filer. In 2023, the 22% bracket started at $44,725. For 2024, that same bracket doesn't kick in until you hit $47,150. That is a $2,425 difference. If you earned $46,000 last year, you were paying 22% on that top slice of income. This year, at that same salary, you’ve actually dropped back down into the 12% bracket for those dollars. It’s a win. Sorta.

Most people get confused about how these calculators work because they think the "bracket" applies to all their money. It doesn’t. We have a progressive system.

Imagine you have three buckets. The first bucket holds about $11,600 and is taxed at 10%. Even if you make a million dollars, that first $11,600 is still only taxed at 10%. The next bucket is taxed at 12%, and so on. When a 2024 tax brackets calculator tells you that you’re in the "24% bracket," it just means your last dollar earned is taxed at that rate. Your effective tax rate—the actual percentage of your total income that goes to the government—is always lower than your bracket.

The Standard Deduction Shift

You can't talk about brackets without talking about the standard deduction. This is the amount of money the IRS basically ignores before they even start looking at your brackets. For 2024, the standard deduction jumped to $14,600 for single filers and $29,200 for married couples filing jointly.

If you’re a married couple making $100,000 total, you don't start paying taxes on $100,000. You subtract that $29,200 first. Now you're looking at $70,800 of taxable income. That is the number you should be plugging into a 2024 tax brackets calculator if you want any semblance of accuracy. If you plug in your gross pay, the tool will give you a terrifyingly high number that isn't real.

Why Your "Refund" Might Be Smaller Than Expected

Here is the weird part. Even though the brackets shifted in a way that favors the taxpayer, your refund might not be bigger. Employers adjust their withholding tables based on these new IRS rules. If your boss's payroll software was updated correctly, they took out less money from your paycheck throughout 2024.

You saw that money in your weekly or monthly pay. You already spent it.

Tax pros like those at Deloitte or the Tax Foundation have noted that while the "tax bite" is technically smaller due to inflation adjustments, many Americans feel like they are paying more because of how expensive everything else is. It’s a psychological disconnect. You’re paying less to Uncle Sam, but the grocery store is taking the difference.

Filing Status Nuances

Your filing status is the biggest lever you have. A head of household—usually a single parent—gets a much better deal than a single person with no kids. For 2024, the head of household standard deduction is $21,900.

👉 See also: BRICS Explained: What the Group Really Stands For and Why It’s Changing Everything

- Single: $14,600

- Married Filing Jointly: $29,200

- Head of Household: $21,900

If you're recently divorced or your living situation changed in 2024, don't just click "single" because it's easy. Check if you qualify for Head of Household. It could move you down an entire tax bracket.

Capital Gains and the "Hidden" Brackets

Not all income is created equal. If you sold stocks or a property you held for more than a year, that money isn't taxed at the standard 10% to 37% rates. It uses the long-term capital gains brackets, which are 0%, 15%, or 20%.

A lot of people don't realize that for 2024, you can actually make up to $47,025 (as a single filer) or $94,050 (married filing jointly) in taxable income and pay zero percent in capital gains taxes. That’s huge. If you’re retired or had a low-income year but sold some winning stocks, you might owe the IRS absolutely nothing on those gains. Most basic tax calculators won't tell you that unless you dig into the "investment income" settings.

Credits vs. Deductions

Deductions (like the standard deduction) lower the income you are taxed on. Credits (like the Child Tax Credit) are way better. They are a dollar-for-dollar reduction of the tax you owe.

For 2024, the Child Tax Credit remains at $2,000 per qualifying child. However, the "refundable" portion—the part you get back even if you owe zero taxes—has been adjusted for inflation to $1,700. If a 2024 tax brackets calculator asks for your number of dependents, make sure you're accurate. Being off by one kid changes your bottom line by thousands.

Common Mistakes When Using Online Tools

Honestly, the biggest mistake is "Garbage In, Garbage Out."

People forget about their side hustles. If you did some DoorDash, sold stuff on Etsy, or did freelance consulting, you have to account for Self-Employment Tax. This is roughly 15.3% on top of your income tax. A standard 2024 tax brackets calculator usually focuses on Federal Income Tax, ignoring the Social Security and Medicare taxes that freelancers have to pay themselves. If you made $10,000 on the side, you might owe $1,500 just in self-employment tax before the income tax even touches it.

Then there is the state tax. Unless you live in a place like Florida, Texas, or Washington, your state is going to want its cut. Most federal calculators won't factor in your state's specific brackets, which can range from a flat 3% to a progressive 13% in places like California.

The Alternative Minimum Tax (AMT)

The AMT is like a "shadow" tax system designed to make sure wealthy people don't use too many deductions to pay nothing. For 2024, the AMT exemption amount increased to $85,700 for singles and $133,300 for married couples. Unless you're making high six figures or have very complex incentive stock options, you probably don't need to worry about this. But if you are in that high-earner category, a simple bracket calculator is going to be completely useless for you. You need a pro.

Real-World Example: The "Middle Class" Squeeze

Let’s look at a couple, "The Millers," filing jointly with two kids. They earned $120,000 in 2024.

- They take the $29,200 standard deduction.

- Their taxable income is now $90,800.

- Looking at the 2024 brackets, they are entirely in the 10% and 12% tiers.

- Their total tax before credits is roughly $10,400.

- They have two kids, so they get $4,000 in Child Tax Credits.

- Their final federal tax bill: $6,400.

In this scenario, their effective tax rate is only 5.3%. That’s a far cry from the "22% bracket" they might have feared they were in.

What You Should Do Right Now

The 2024 tax year is over, but the filing season is just starting.

First, grab your last pay stub from December 2024. It will show your total gross pay and, more importantly, how much federal tax was already withheld.

Second, don't just use one 2024 tax brackets calculator. Try two or three. Compare the results. If one says you owe $5,000 and another says you're getting a $2,000 refund, look at how they are handling "Adjusted Gross Income."

Third, check your eligibility for the Earned Income Tax Credit (EITC). For 2024, the maximum credit is $7,830 for those with three or more children. This is one of the most overlooked "big money" items for low-to-moderate-income earners.

Finally, get your documents organized. If you’re itemizing—which is rare now since the standard deduction is so high—you need receipts for everything: mortgage interest, state and local taxes (up to $10,000), and charitable gifts. Most people are better off taking the standard deduction, but it's worth doing the math if you had massive medical bills (over 7.5% of your income) or huge donations.

The IRS website (IRS.gov) has its own withholding estimator which is essentially the gold standard of calculators. It’s a bit clunky, but it’s the most "official" way to see where you stand before you hit "submit" on your tax software.

Adjust your expectations. The 2024 brackets are wider, the deductions are higher, and the credits are adjusted. It’s a year of "more," but given how much the price of eggs and gas went up, that "more" might just keep you level with where you were two years ago. Stay on top of the paperwork and don't wait until April 14th to find out you owe money. Generally speaking, the earlier you file, the faster you get your money back, and the less time identity thieves have to try and file a fake return in your name.

Check your 1099s, double-check your W-2s, and make sure you aren't leaving money on the table.