Everyone is staring at Jerome Powell like he’s holding a winning lottery ticket he refuses to cash. If you’ve checked your credit card statement or tried to look at mortgage rates lately, you know why. It's brutal out there. The big question—will interest rates go down—isn't just a matter of curiosity for Wall Street traders; it’s a survival question for anyone trying to buy a house or keep a small business afloat in 2026.

Prices are weird. Honestly, the economy is acting like a car that’s idling too high. The Federal Reserve spent the last couple of years slamming on the brakes to stop inflation from turning us into a cautionary tale from the 1970s. They succeeded, mostly. But now we’re stuck in this awkward waiting room where money is expensive and everyone is holding their breath.

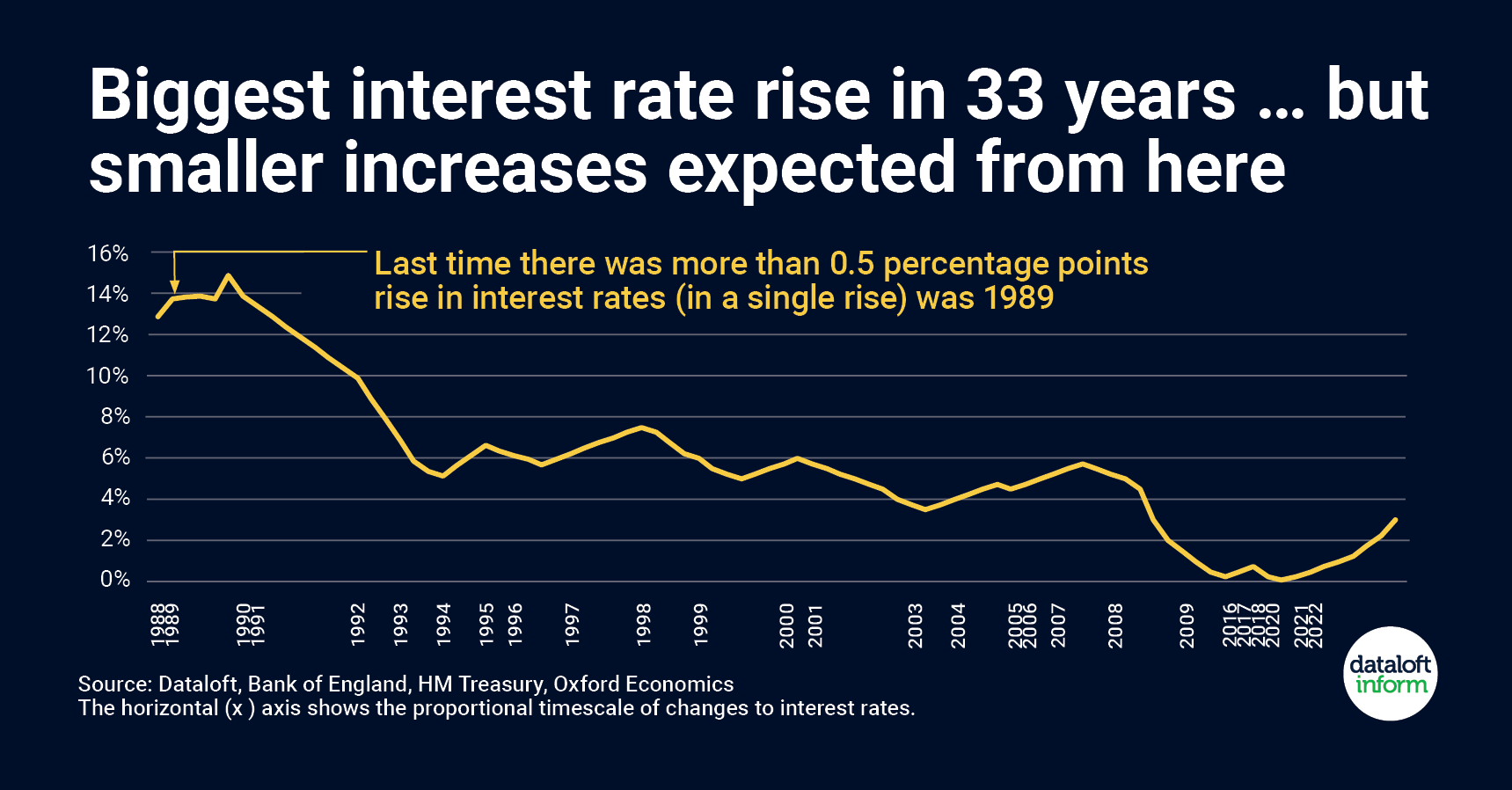

Why the Fed is being so stubborn about cuts

You’ve probably heard the term "data-dependent" until you’re blue in the face. It’s the Fed’s favorite shield. Basically, it means they won’t move until the numbers give them a green light, and those numbers have been inconsistent. One month the labor market looks like it’s finally cooling off, and the next, we see a massive surge in hiring that makes the Fed worry about a second wave of inflation.

Jerome Powell knows that if he cuts too early, he risks a rebound in prices. That would be a disaster for his legacy. Think about the "Volcker Era." Paul Volcker had to crush the economy to save it. Powell doesn't want to go that far, but he’s terrified of being the guy who let inflation slip through his fingers twice.

👉 See also: S\&P 500: What Most People Get Wrong About the World's Favorite Index

It's a tightrope. A really thin one.

The ghost of the "Sticky" CPI

Consumer Price Index (CPI) data is the bogeyman here. While the cost of a gallon of milk might have leveled out, "services" inflation is a different beast. We’re talking about insurance premiums, medical care, and rent. These things don’t just drop overnight. Because wages grew significantly over the last few years, people have more money to spend on these services, which keeps the pressure on.

When will interest rates go down for real?

Market analysts at places like Goldman Sachs and J.P. Morgan have been shifting their goalposts constantly. At the start of the year, everyone was betting on a cut by spring. Then it was summer. Now, the consensus is leaning toward a slow, grinding descent rather than a sharp drop.

Don't expect a return to the 2% or 3% mortgage days. Those were an anomaly. A "normal" interest rate environment is likely where we’re headed, which feels high because we’ve been spoiled by a decade of free money.

The global influence

We aren't an island. The European Central Bank (ECB) and the Bank of England are dealing with their own messes. Sometimes they move first, which puts pressure on the U.S. dollar. If the Fed keeps rates high while Europe cuts, the dollar gets even stronger. That sounds good for your summer vacation in Italy, but it’s tough on American companies trying to sell stuff overseas.

Oil prices are the wild card. If geopolitical tensions in the Middle East or Eastern Europe spike, energy prices go up. When energy goes up, everything goes up. The Fed sees that and keeps the "higher for longer" sign flipped on.

The housing market stalemate

If you’re waiting for will interest rates go down to finally trigger a house hunt, you’re in a crowded boat. This is the "lock-in effect." Millions of homeowners are sitting on 3% mortgages and they are never, ever leaving unless they absolutely have to.

This has created a supply desert.

- New construction is trying to fill the gap, but builders are paying high interest on their loans too.

- First-time buyers are getting squeezed from both ends: high prices and high borrowing costs.

- Sellers are scared to become buyers.

Even a small 0.5% drop in rates could unleash a flood of buyers who have been waiting on the sidelines. Ironically, that surge in demand might just push home prices even higher, neutralizing the benefit of the lower rate. It's a bit of a "pick your poison" scenario.

What it means for your wallet today

Credit card debt is the silent killer right now. With APRs hovering near record highs, carrying a balance is essentially lighting money on fire. If you're waiting for the Fed to save you, stop. Even if they cut rates by 25 or 50 basis points, your credit card interest rate is still going to be astronomical.

- High-Yield Savings Accounts: This is the silver lining. For the first time in forever, you can actually earn 4% or 5% just by letting your money sit in a boring savings account. If rates do go down, these yields will be the first thing to vanish.

- Refinancing Dreams: Keep your credit score pristine. When the window opens—and it will—you need to be ready to jump.

- Fixed vs. Variable: In this environment, "variable" is a dirty word. Lock in what you can, but stay flexible for the long term.

The "Soft Landing" obsession

The Fed wants a soft landing. That’s the holy grail of economics—bringing inflation down without causing a massive recession and 10% unemployment. So far, the labor market has been surprisingly resilient. People are still working. They are still spending, though maybe they're switching from name-brand cereal to the store brand.

✨ Don't miss: Christopher Ivey MC AI Arbitrage: What Most People Get Wrong

But there’s a lag.

Interest rate hikes usually take 12 to 18 months to fully soak into the economy. We might still be feeling the effects of hikes that happened a year ago. That’s why the Fed is being so cautious. They don't want to oversteer the ship into an iceberg they didn't see because they were too busy looking at last month's grocery prices.

Practical steps to take while waiting

Stop checking the news every five minutes for a Fed announcement. It’s bad for your blood pressure. Instead, look at your own balance sheet.

Prioritize high-interest debt immediately. If you have a loan with a variable rate, see if you can consolidate it into a fixed-rate personal loan now. Even if the rate feels high, the certainty is worth something.

Lock in your savings rates. If you have cash sitting in a standard checking account, move it to a CD (Certificate of Deposit) or a high-yield savings account today. If rates start to tumble, banks will drop their payout rates faster than a hot potato. By locking in a 12-month CD now, you're guaranteed that return even if the Fed starts slashing rates in six months.

🔗 Read more: How Much of 1099 Income Is Taxed: What Most People Get Wrong

Watch the 10-Year Treasury Yield. This is the real secret. Mortgage rates aren't directly set by the Fed; they track the 10-year Treasury. When you see that yield start to dip, that’s your signal that the market thinks a rate cut is coming. It’s often a leading indicator that gives you a few weeks' head start on the rest of the public.

Audit your subscriptions and "lifestyle creep." When money was cheap, we all got a bit lazy. In a high-interest world, cash flow is king. Tightening the belt now means that when will interest rates go down finally becomes "interest rates are down," you’ll have the capital ready to invest when everyone else is still trying to dig out of their holes.

The reality is that we are likely entering a period of "higher for longer" than most of us want to admit. The days of 0% interest rates were a historical freak accident, and they aren't coming back anytime soon. Prepare for a world where money has a real cost, and you'll be ahead of 90% of the population.