If you’re waiting for mortgage rates to tumble back to those 3% pandemic-era basements, I have some news that might sting. It isn’t happening. Honestly, anyone promising a return to those rates is probably trying to sell you a dream that the current economy just can't support.

But here is the twist. Will mortgage rates drop at all this year? Yes, they probably will, but it’s going to be a slow, grinding descent rather than a freefall. We’re currently in early 2026, and the 30-year fixed rate is finally hovering around the 5.8% to 6.2% range. It’s a psychological victory for anyone who sat through the 7% spikes of 2024 and 2025.

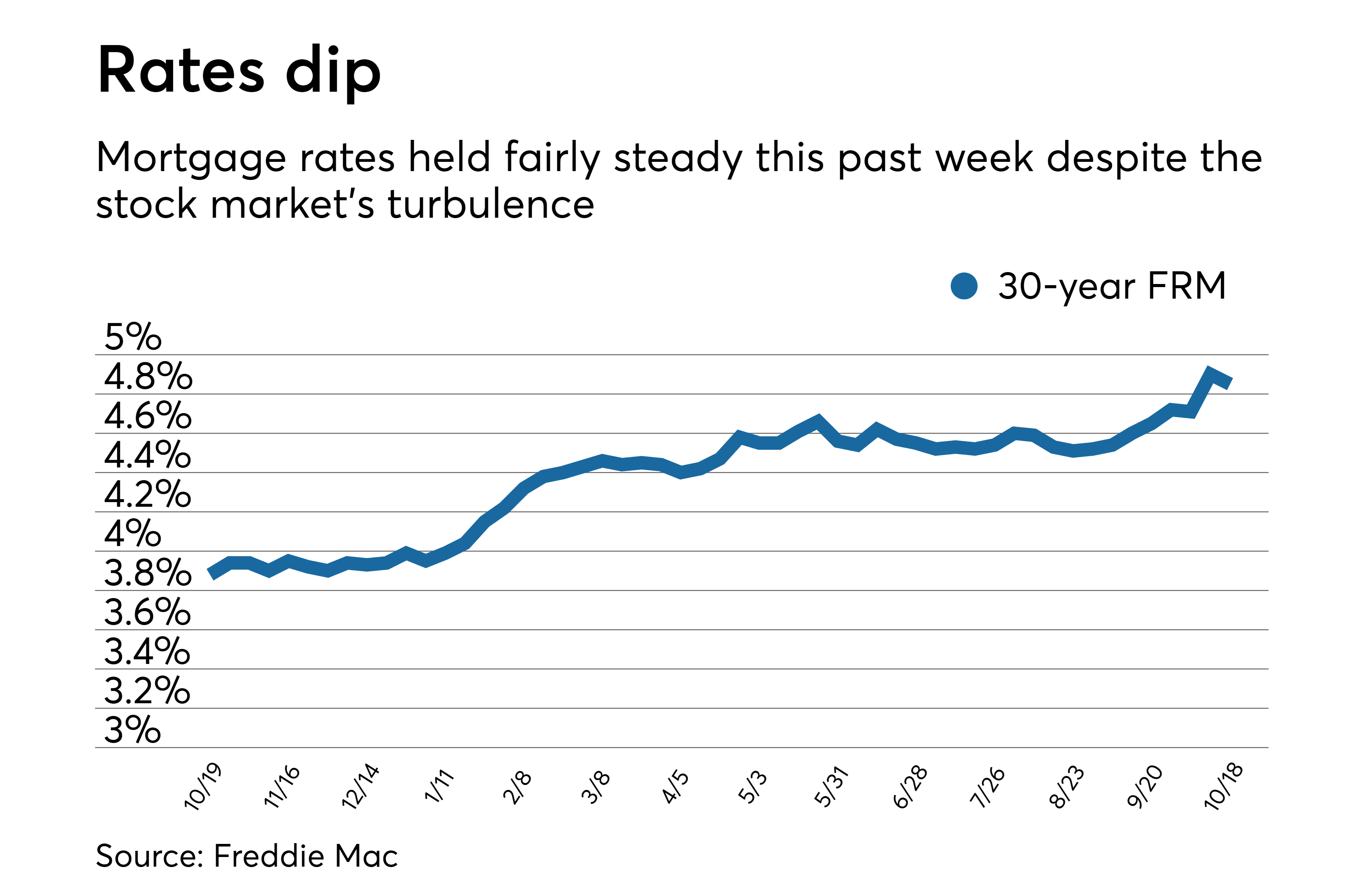

The market is weird right now. One day you see a "welcome dip" below 6%, and the next, a sticky inflation report sends the 10-year Treasury yield—and your potential monthly payment—climbing back up.

Why the "Fed Cut" Magic Isn't Working Like You Think

There’s this massive misconception that the Federal Reserve "sets" mortgage rates. They don't. The Fed sets the federal funds rate, which is basically the price banks pay to lend each other money overnight. While that trickles down, mortgage rates actually prefer to dance with the 10-year Treasury yield.

Lately, that dance has been awkward.

In late 2025, the Fed cut rates by a full point over three meetings, but mortgage rates actually rose during part of that window. Why? Because investors were nervous about long-term inflation and government debt. If the people buying mortgage-backed securities think prices will stay high, they demand a higher return. This is why you can’t just watch the Fed and assume your house is getting cheaper.

The 2026 Forecast Breakdown

Experts are currently split, which is always fun for your stress levels. Here is the gist of what the big players are saying for the rest of 2026:

- Fannie Mae is feeling optimistic, eyeing a dip toward 5.9% by the end of the year.

- The Mortgage Bankers Association (MBA) is playing it safer, predicting we stay closer to 6.4%.

- Bankrate’s Ted Rossman thinks we might see 5.5% if the economy cools too fast, but that’s a "best-case" scenario.

- J.P. Morgan threw a wrench in everything recently by suggesting the Fed might not cut at all in 2026 if the job market stays this tight.

Basically, we are looking at a "new normal" where 5.5% is the new 3%. It’s sort of frustrating, but it’s the reality of a 2026 economy that is still shaking off the cobwebs of the last few years.

The Inflation Ghost is Still Haunted

Inflation is the ultimate vibe-killer for mortgage rates. Even though we’ve seen it cool down significantly from the scary peaks, it’s still hovering slightly above that 2% target the Fed loves so much.

When you go to the grocery store and realize your $100 cart is now $130, you're seeing why lenders are hesitant. High prices mean the Fed has to keep the brakes on the economy. If they let off too soon, inflation could flare up again, and mortgage rates would respond by shooting back toward 7% faster than you can say "pre-approval."

💡 You might also like: The Real Definition of Collusion and Why It Costs You Money

The "Lock-In" Effect is Finally Cracking

For the last couple of years, people were trapped. If you had a 2.5% rate from 2021, why would you sell and buy a new place at 7%? You wouldn’t. You’d stay put and renovate the basement.

But something is changing in 2026. We’re seeing "mortgage swappers" emerge. These are people who have realized that waiting for 3% is a fool’s errand. They’re finally listing their homes because they need more space or a new job, and a 5.8% rate feels "good enough" compared to the 7.5% they saw a year ago. This is finally putting some inventory back on the market, though not enough to cause a price crash.

What This Means for Your Wallet

If you’re sitting on the sidelines, you have to weigh the "rate vs. price" trap.

When rates drop, more buyers jump in. More buyers mean more competition. More competition means home prices go up. If you wait for rates to drop another 0.5%, but the house price goes up by $30,000 in that time, did you actually win? Probably not.

For those looking to refinance, the window is finally opening for anyone who bought in 2023 or 2024 at those 7% or 8% peaks. If you can shave 1% or 1.5% off your rate, the math usually checks out, even with closing costs.

👉 See also: John E. Jenkins Inc: The Real Story Behind the Specialized Construction and Environmental World

Actual Next Steps for 2026 Borrowers

- Stop timing the bottom. You won't catch it. If you find a house you love and the payment doesn't make you cry, that's your signal.

- Watch the 10-year Treasury, not just the news. When the yield on the 10-year drops, mortgage lenders usually follow suit within 24 to 48 hours.

- Check your credit score today. In this environment, the gap between "good" and "excellent" credit can be the difference between a 5.9% and a 6.5% rate. That’s hundreds of dollars a month.

- Look into 5/1 ARMs. They’ve become popular again. If you plan on moving in a few years anyway, an Adjustable-Rate Mortgage might give you a lower entry point while we wait for the long-term market to settle.

The era of "free money" is over. We’re settling into a period where mortgage rates are stable but "expensive" compared to our recent memories. It’s not the news everyone wants, but it’s the stability the market needs to stop being so volatile. If you're waiting for a sign, this slow drift downward is likely as good as it gets for the foreseeable future.

Practical Actions to Take Now:

Calculate your "break-even" point for a refinance if your current rate is above 7.2%. Many lenders are now offering "no-cost" refinance options to capture the 2026 volume, which can save you from paying thousands in upfront fees. If you are a buyer, get a "locked-in" pre-approval that allows you to "float down" if rates drop before you close. This gives you the protection of a ceiling with the benefit of a floor.