Investing feels like a chaotic game of chance until someone hands you a map. For most of us in the finance world, that map—despite its many wrinkles and tears—is the CAPM model. It’s the Capital Asset Pricing Model.

Honestly? It's kind of old.

Jack Treynor, William Sharpe, John Lintner, and Jan Mossin started piecing this thing together in the early 1960s. They wanted to solve a single, nagging problem: How much return should you actually demand for taking on a specific amount of risk? If you’re putting your hard-earned money into a volatile tech stock versus a sleepy utility company, you shouldn't expect the same payout. CAPM gives you a number. It’s the "required rate of return."

The CAPM Model and the Price of Risk

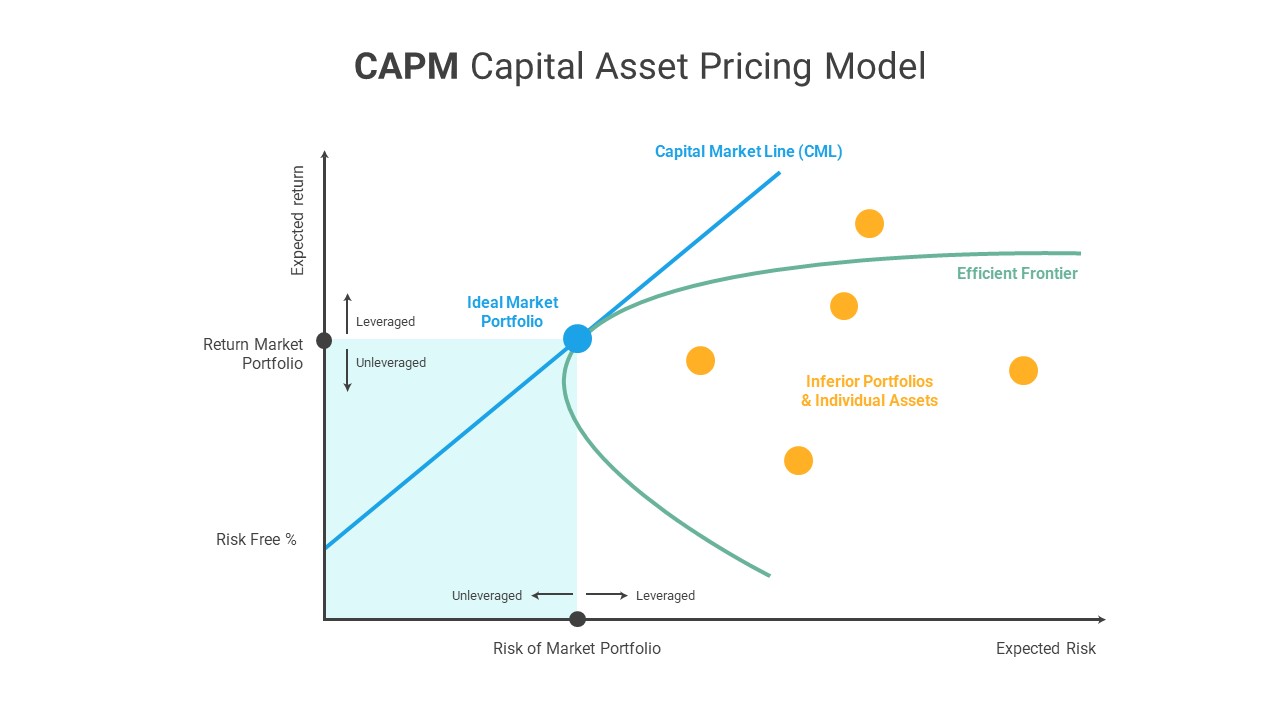

The beauty of the CAPM model lies in its simplicity. It argues that the return on any asset is basically the sum of a "risk-free" rate plus a premium for taking a gamble.

Think of it like this. You could put your money in 10-year U.S. Treasury bonds. Those are widely considered the "risk-free" benchmark because, well, the government can just print more money to pay you back. If that bond pays you 4%, that’s your floor. You wouldn’t invest in a risky startup for 4%. You’d want 4% plus something extra to compensate you for the sleepless nights.

That "something extra" is the risk premium.

The Formula You’ve Seen Everywhere

You’ll see it written out as:

$$E(R_i) = R_f + \beta_i (E(R_m) - R_f)$$

It looks intimidating. It isn't.

- $E(R_i)$: This is what you’re looking for. The expected return.

- $R_f$: The risk-free rate (like that Treasury bond).

- $\beta_i$: Beta. This is the "sensitivity" knob. It measures how much the stock moves compared to the overall market.

- $E(R_m) - R_f$: The Market Risk Premium. This is just the extra return the whole stock market provides over the risk-free rate.

If a stock has a Beta of 1.0, it moves perfectly in sync with the market. If the market goes up 10%, the stock goes up 10%. If Beta is 2.0? The stock is a roller coaster. It might jump 20% when the market only moves 10%. But it’ll also crash twice as hard.

Why Beta is the Only Risk That Matters (According to CAPM)

Here is where it gets a bit controversial. The CAPM model makes a massive assumption. It claims that there are two types of risk: systematic and unsystematic.

🔗 Read more: Family Office News Asia: What Most People Get Wrong About the 2026 Wealth Shift

Unsystematic risk is stuff specific to a company. A CEO gets fired. A factory burns down. A product recall happens. CAPM says you shouldn't get paid for taking this risk. Why? Because you can "diversify" it away. If you own 50 different stocks, one factory fire doesn't ruin your life.

Systematic risk is the scary stuff. It’s recessions, wars, interest rate hikes, and global pandemics. You can’t hide from it. Since you can’t diversify away from the "market," the model says this is the only risk you should actually be compensated for.

That’s what Beta measures. It ignores the factory fire and focuses only on the market-wide earthquake.

The Real World vs. The Model

Is CAPM perfect? Not even close.

Fama and French, two legendary researchers, famously threw a wrench in the gears back in the 90s. They pointed out that Beta doesn't explain everything. Small-cap stocks and "value" stocks (ones that look cheap) often outperform what the CAPM model predicts they should do.

✨ Don't miss: Why Colorado Fuel and Iron Still Matters: The Messy History of the Industrial West

There are also the "unrealistic" assumptions. The model assumes:

- You can borrow and lend at the risk-free rate (you can’t; your bank definitely charges you more than the government).

- There are no taxes or transaction costs (tell that to the IRS).

- Everyone has the same information at the same time.

- Investors are totally rational.

We know people aren't rational. We know markets get emotional. Yet, we still use CAPM.

Why? Because it’s a brilliant starting point. When a CFO needs to decide whether to build a new billion-dollar semiconductor plant, they need a "hurdle rate." They need to know if the project's returns beat the cost of the capital. CAPM provides that benchmark. It’s the industry standard for a reason: it’s easy to communicate and it captures the fundamental truth that higher risk should equal higher reward.

Applying the CAPM Model to Your Portfolio

Let's do a quick, real-world scenario.

Imagine the 10-year Treasury is at 4.2%. You're looking at a tech stock with a Beta of 1.3. Historically, the S&P 500 returns about 10%.

Using the CAPM model, your expected return would be:

$4.2% + 1.3 \times (10% - 4.2%) = 11.74%$

If you think that stock is only going to return 9% next year, CAPM is telling you it's a bad deal. You aren't being paid enough for the risk you're shouldering. You might as well buy a lower-beta stock or stick with an index fund.

Practical Steps for Investors

Don't just stare at the formula. Use it to audit your thinking.

- Check your Beta. Look up the Beta of your largest holdings on a site like Yahoo Finance or Bloomberg. If your entire portfolio is full of 1.5+ Beta stocks, realize you aren't "beating the market"—you’re just leveraging yourself to it. When the wind changes, you'll feel it more than others.

- Evaluate the Risk-Free Rate. In a high-interest-rate environment, the "bar" for stocks is higher. When Treasuries pay 5%, a stock promising 7% is barely worth the risk.

- Don't ignore the "Unsystematic" stuff. Remember that CAPM assumes you are diversified. If you only own three stocks, the "factory fire" risk that CAPM ignores could still wipe you out.

- Use it as a "sanity check." If an investment advisor promises you 15% returns on a "low-risk" asset, run the CAPM numbers. If the math doesn't align with the risk-free rate and the market premium, someone is likely lying to you.

The CAPM model isn't a crystal ball. It’s a compass. It won't tell you exactly where the cliff is, but it'll definitely tell you which way is north. Use it to set your expectations, calculate your hurdle rates, and keep your risk in perspective.

Actionable Next Steps:

- Identify your personal "hurdle rate" by adding the current 10-year Treasury yield to a standard 5-6% equity risk premium.

- Audit your brokerage account to see if your average Beta aligns with your actual stomach for volatility.

- Compare the CAPM expected return of your favorite individual stock against its actual 5-year historical performance to see if it has historically "earned" its risk premium.