Death and taxes. You've heard the cliché a thousand times. But honestly, most people don't realize that where you decide to spend your golden years can drastically change how much of your hard-earned money actually makes it to your kids.

Federal taxes get all the headlines. We talk about the big $15 million exemption for 2026, which feels like plenty of breathing room for almost everyone. But then there’s the "stealth tax."

The state-level bite.

🔗 Read more: 90000 MXN to USD: Why Your Bank Is Probably Robbing You

Depending on where you live, estate tax rates by state can kick in at much lower levels than the federal government’s threshold. Some states start taking a cut when you hit just $1 million. In a world where a modest three-bedroom home in a good neighborhood can easily clear $800,000, you’re suddenly a "wealthy" estate in the eyes of the tax man.

The 2026 Landscape: It’s Not Just One Big Number

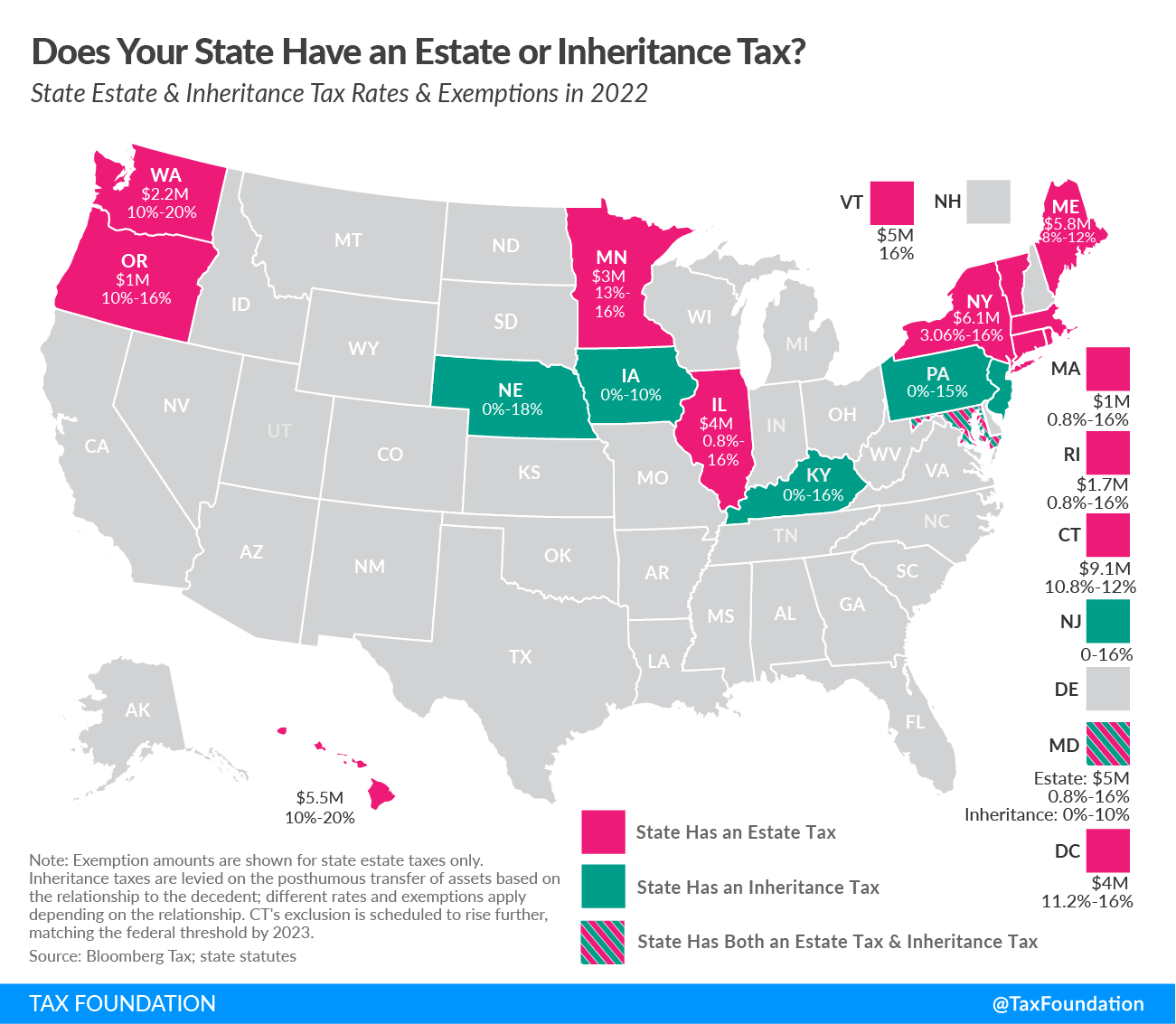

Right now, we are looking at a weirdly fragmented map. Most states—37 of them, to be exact—don't have an estate tax at all. If you live in Florida or Texas, your heirs are basically doing a victory dance. But if you’re in the Northeast or the Pacific Northwest, things get complicated.

Here is the thing: some states have an estate tax, while others have an inheritance tax. They sound like the same thing, but they aren’t. An estate tax is taken out of the pile of money before it's handed out. An inheritance tax is a bill your daughter or nephew gets after they receive the cash.

Maryland is the "winner" of the most confusing award. It’s the only state that hits you with both.

The States That Still Take a Cut

Let’s look at the actual numbers for 2026. This isn't just dry policy; it's the difference between leaving a legacy and leaving a legal headache.

📖 Related: Dan Quayle Net Worth: Why the Former VP Is Way Wealthier Than You Think

- Oregon: This is the big one people miss. The exemption is stuck at $1 million. If your house and your 401(k) add up to $1.1 million, Oregon wants a piece. Rates go from 10% up to 16%.

- Massachusetts: They recently bumped their threshold to $2 million. It used to be $1 million, so this was a huge relief for residents, but it’s still a far cry from the federal $15 million.

- Washington State: Things just got interesting here. For 2026, the exemption jumped to $3 million, but they also hiked the top tax rate to a staggering 35% for the biggest estates.

- New York: The "Cliff" state. New York has an exemption of $7.35 million for 2026. But here is the trap: if you go even 5% over that limit, the state taxes the entire amount, not just the extra bit. It’s a brutal mathematical cliff.

- Illinois: Still holding steady at a $4 million exemption with a top rate of 16%.

The Inheritance Tax Outliers

Inheritance taxes are arguably more "personal" because the rate often depends on who is getting the money. If you leave money to a spouse, it's almost always tax-free. If you leave it to a random friend or a distant cousin? That’s when the rates spike.

- Nebraska: They have some of the highest inheritance tax rates for "remote" relatives, though they’ve been working on gradual reductions.

- Pennsylvania: No estate tax, but a very active inheritance tax. Even a 4.5% rate on transfers to children can add up to tens of thousands of dollars.

- New Jersey: They abolished their estate tax years ago but kept the inheritance tax.

- Kentucky and Iowa: Both have specific rules that favor immediate family but can be pricey for "Class C" beneficiaries (unrelated people).

Why the Federal "Big Beautiful Bill" Changed the Game

You might have heard about the "sunset" that was supposed to happen. For years, planners warned that the federal exemption would drop by half in 2026.

It didn't happen.

The 2025 legislative changes (often called the "Big Beautiful Bill" or OBBBA) made the high exemptions permanent. For 2026, the federal exemption is $15 million per person. If you’re married, you’re looking at $30 million.

This is massive. It means for the vast majority of Americans, the federal government isn't the problem. The state is.

If you live in Oregon with a $5 million estate, you owe $0 to the IRS. But you owe Oregon over $400,000. That’s a lot of money to lose just because of a state line.

The Strategy: How People Are Fighting Back

People aren't just sitting around waiting to be taxed. Expert estate planners are using a few specific "moves" to side-step these state-level traps.

The "Snowbird" Residency Flip

This is the classic. You move to Florida or Arizona. But you can't just buy a condo and call it a day. The "tax-heavy" states like New York or Minnesota will fight you. They look at where you vote, where your car is registered, and how many days you actually spent in the state. If you aren't careful, they’ll claim you’re still a resident and tax your global estate anyway.

The Three-Year Gift Rule

In New York, they have a "look-back." If you give away a million dollars and die two years later, New York acts like you still have that money and taxes it. You have to outlive your gifts by three years to truly clear them from your New York estate.

The SLAT (Spousal Lifetime Access Trust)

This is a bit nerdy but very effective. You put money into an irrevocable trust for your spouse. You lose direct ownership (which keeps it out of your estate), but your spouse can still access the money for their needs. It's a way to "freeze" the value of your assets so the state can't tax the future growth.

Real Talk: Is It Worth Moving?

Honestly? It depends.

If you have $2 million and live in Massachusetts, your state tax bill might be around $100,000. Is it worth leaving your friends, your doctors, and your grandkids to save $100k? Probably not.

But if you’re in Washington State with $15 million, you’re looking at a tax bill in the millions. At that point, a U-Haul starts looking pretty attractive.

The biggest mistake I see is people assuming that because they are "under the federal limit," they don't need a plan. That is how the states get you. They rely on that complacency.

Your 2026 Action Plan

If you think you might be over your state's threshold, don't panic. But don't wait.

💡 You might also like: 1200 Pesos to Dollars: What You're Actually Getting After Fees

- Check the Title: Sometimes simply moving a house into a specific type of trust can mitigate the "cliff" effect in states like New York.

- Annual Gifting: You can give away $19,000 per person in 2026 without even filing a tax return. If you and your spouse give that to your two kids and their spouses, that’s $152,000 out of your taxable estate every single year.

- Update Your Will: If your will was written in 2015, the "formula clauses" inside it might be completely broken for the 2026 tax laws.

The estate tax rates by state are a moving target. What's true in January might be changed by a late-session budget bill in June. Stay local, stay informed, and remember that "permanent" in tax law usually just means "until the next election."

Actionable Next Steps:

- Calculate your "Gross State Estate": Don't just look at cash. Include life insurance payouts (which are often taxable at the state level), your home's current market value, and all retirement accounts.

- Map your heirs: If you live in an inheritance-tax state like Pennsylvania or Nebraska, categorize your beneficiaries by "Class." Knowing that a nephew is taxed at a higher rate than a son can change how you allocate specific assets.

- Consult a state-specific pro: A federal tax expert in Texas won't know the nuances of the Oregon "Oregon-only" QTIP election. Get someone who knows your local courthouse.