If you’ve been watching the koninklijke philips share price lately, you know it feels a bit like watching a high-stakes medical drama. One minute the patient is stable; the next, there’s a frantic beeping in the corner of the room.

Honestly, the ticker (PHG on the NYSE or PHIA in Amsterdam) has been a wild ride. As of mid-January 2026, the stock is hovering around the $29.50 to $30.00 mark. That’s a massive leap from the dark days of 2022 and 2023 when the sleep apnea recall seemed like it might swallow the company whole.

But here’s the thing. Most people looking at the charts are missing the "reconstruction" story happening under the hood.

The Ghost of the DreamStation Recall

You can't talk about the stock without talking about the foam. For years, Philips was anchored by a massive recall of its DreamStation CPAP machines. The polyester-based polyurethane foam was degrading, and investors were terrified of an "endless litigation" scenario.

Fast forward to now. Philips basically settled a huge chunk of that headache in 2024 with a $1.1 billion agreement for personal injury claims in the US. While that sounds like a staggering amount of money, the market actually exhaled. Why? Because it wasn't $5 billion. It wasn't $10 billion. It was a known, manageable number.

Current sentiment is largely driven by the fact that the "litigation floor" has been set. We aren't guessing in the dark anymore. The company is currently rolling out payments through 2025 and 2026, and while the legal shadow hasn't completely vanished, it’s much thinner than it used to be.

Why February 10, 2026, Is the Only Date That Matters

If you're holding or eyeing the stock, circle February 10 on your calendar. Philips is scheduled to release its Q4 and full-year 2025 results, but more importantly, they are dropping their official 2026 outlook.

🔗 Read more: Stock chart candle patterns: What most people get wrong about reading the tape

Management has already been dropping breadcrumbs. They’ve reiterated they expect "mid-single-digit" growth. Not double-digit, world-changing growth—just steady, boring, reliable growth. In the world of medical tech, "boring" is actually a compliment.

The Real Numbers Right Now:

- Current Price: Roughly $29.58 (as of Jan 16, 2026).

- 52-Week Range: $21.48 – $30.30.

- Dividend Yield: Sitting around 3.27%.

- P/E Ratio: Still looking a bit inflated at 146x on a trailing basis, but the forward P/E is a much more grounded 16.7x.

The 52-week high is right within reach. If the February announcement shows that margins are expanding despite the global "tariff headaches" everyone is talking about, we might see the price break into the $30s for the first time in a long while.

The "New" Philips: AI and Shaved Heads

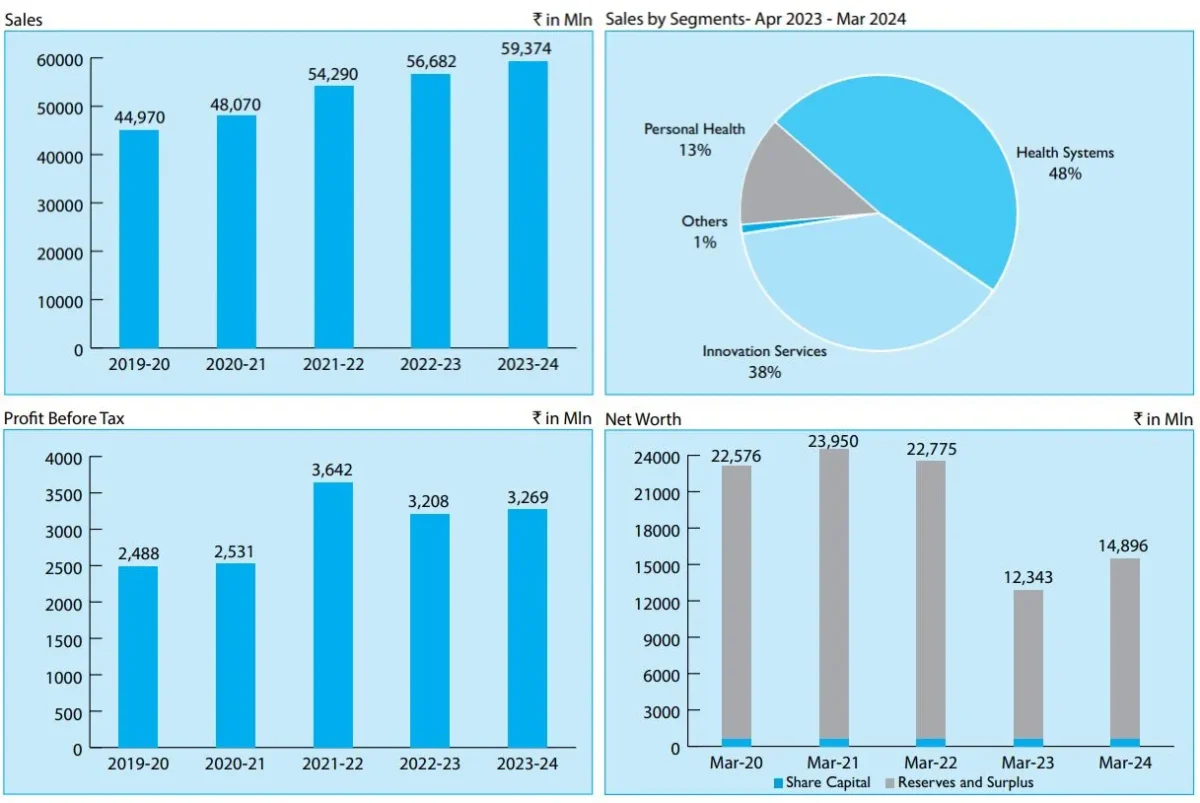

It's sorta funny—people forget Philips still sells electric razors. Their Personal Health segment, which includes things like the Norelco line and the Lumea IPL hair removal tech, grew by 11% in late 2025. That’s the "cash cow" that keeps the lights on while the high-end hospital tech (Diagnosis & Treatment) deals with longer sales cycles.

The real "expert" play here is watching their AI integration. They recently launched a platform called LumiGuide, which uses light-based 3D navigation for surgeries. This isn't just a gadget; it's a way to keep doctors from getting blasted with X-ray radiation.

Hospitals are buying into this "as-a-service" model. Instead of just buying a machine, they are signing long-term "Enterprise Monitoring" deals. This creates recurring revenue, which is exactly what stock analysts love to see because it makes future earnings more predictable.

The Risks Nobody Mentions

Don't let the recent rally fool you into thinking it's all sunshine. There are still some "gotchas."

First, the Consent Decree with the US Department of Justice. Philips is still restricted in how it can sell certain sleep and respiratory products in the US. They aren't fully "back" in that market yet.

Second, there's the China factor. Like every other global healthcare giant, Philips is feeling the "China chill"—a mix of local competition and government procurement changes that make it harder to sell expensive MRI machines there.

Lastly, there’s the "Tariff Headwind." CEO Roy Jakobs has been vocal about navigating an uncertain macro environment. If new trade barriers go up, those margins they worked so hard to fix could get squeezed again.

✨ Don't miss: 5088 W Innovation Circle Phoenix AZ: What Business Owners Get Wrong About This Tech Hub

What to Actually Do

If you’re looking at the koninklijke philips share price as a long-term play, the focus shouldn't be on the daily swings. You have to look at the productivity program. They are on track to save about EUR 2.5 billion through cost-cutting and efficiency.

- Watch the Cash Flow: They're targeting free cash flow in the EUR 0.2–0.4 billion range. If they beat this in February, the stock likely pops.

- The "Litigation Tail": Keep an eye on any new class actions outside the US. While the US settlement was the big one, global echoes can still cause volatility.

- February 10 Catalyst: This is the make-or-break day for the 2026 trajectory.

Next Steps for Investors: Log into your brokerage and set a price alert for $30.30. That is the current 52-week resistance level. If the stock breaks and holds above that following the February 10th outlook, it signals that the market has finally moved past the recall era and is pricing Philips as a growth-oriented health-tech leader again. You should also pull the Q3 2025 report from the Philips Investor Relations site to see the segment-by-segment margin improvements for yourself—specifically the Connected Care turnaround.