So, you've been watching the Power Finance Corporation Ltd stock price lately. It’s been a bit of a rollercoaster, right? One day it's pushing toward the ₹380 mark, and the next, it’s slipping back toward ₹360 like someone pulled the plug. Honestly, if you're just looking at the daily ticker, you’re missing the actual chess game being played here.

This isn't just another boring state-owned enterprise (PSU) stock that sits in your grandfather's portfolio gathering dust. We’re talking about a Maharatna company that basically acts as the backbone for India’s massive energy transition. But let's get real for a second. The market is fickle. While the Power Finance Corporation Ltd stock price closed around ₹371.85 on January 14, 2026, the sentiment is a weird mix of "buy the dip" and "wait for the policy."

The Current Vibe of the PFC Ticker

If you look at the 52-week range, we've seen a high of ₹444.1 and a low of ₹329.9. That’s a massive spread. Most people get spooked by that 15-20% drop from the highs, thinking the party is over. But here’s the thing: PFC is currently trading at a Price-to-Earnings (P/E) ratio of roughly 4.9.

Think about that.

👉 See also: Why Cut the Head Off the Snake Strategies Fail More Often Than They Work

A company that’s growing its net profit by nearly 9% year-on-year (reaching ₹7,834 crore in Q2 FY26) is being valued like it’s a dying business. It's kinda wild. You’ve got a dividend yield sitting around 4.4%, which is basically the stock market's way of paying you to be patient.

Why the Price is "Stuck" (Sorta)

- The Infrastructure Pivot: PFC is moving beyond just power. They've dipped their toes into logistics and general infrastructure, with about ₹14,700 crore already deployed there. Markets hate uncertainty, and some investors are still figuring out if PFC can lend to a highway project as well as they lend to a dam.

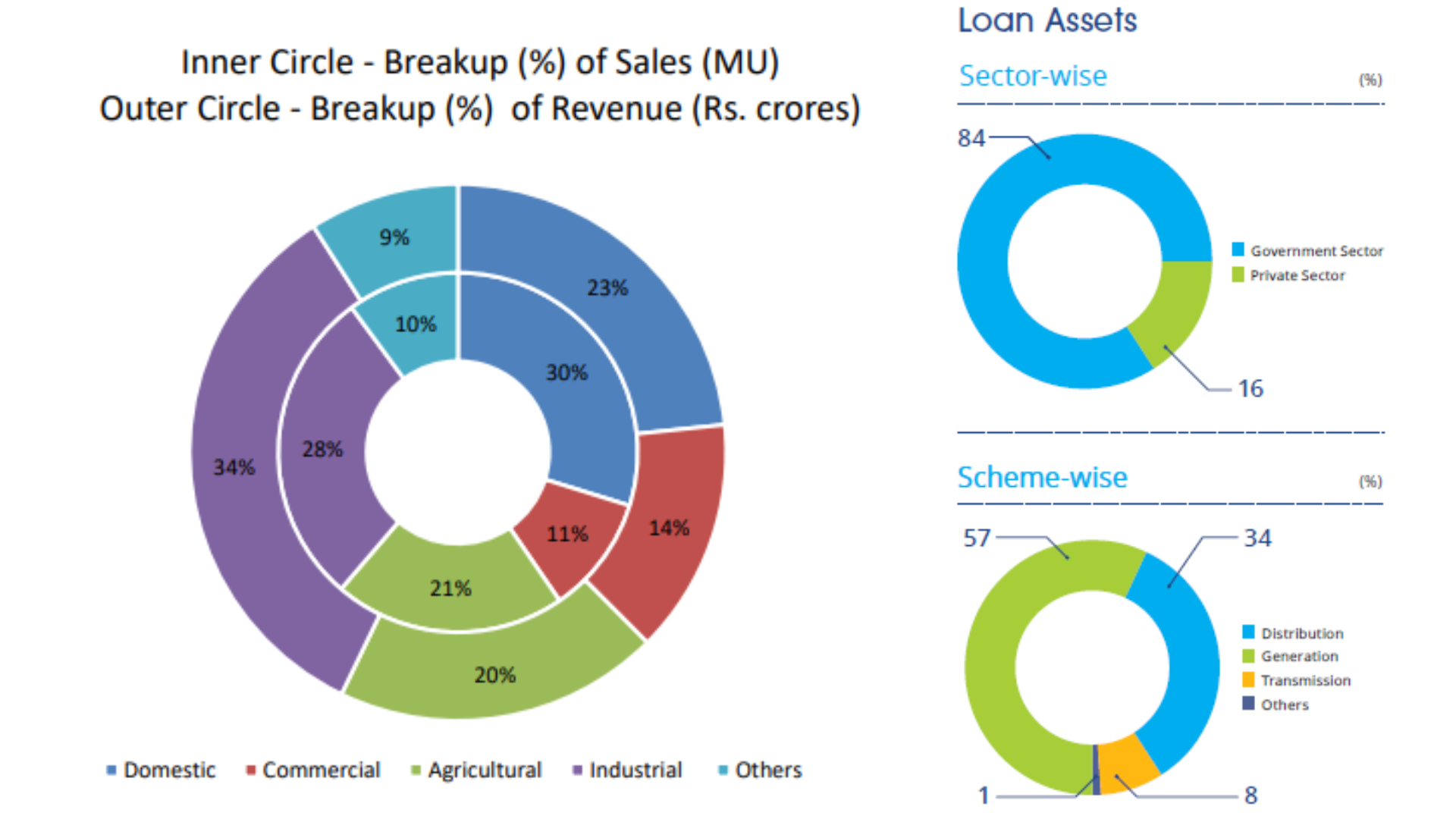

- Asset Quality Ghost Stories: For years, everyone was terrified of "stressed assets" in the power sector. But Chairperson Parminder Chopra recently pointed out that their net Non-Performing Assets (NPAs) have plummeted to a tiny 0.37%. Most of the bad debt is from old private sector thermal projects that are already 80% provided for or in liquidation.

- The Nuclear Wait-and-Watch: There’s buzz about PFC funding nuclear power projects. The government has this ambitious 100 GW target for 2047. But PFC is being smart—they aren't jumping in until the policy framework is crystal clear. This "cautious optimism" often keeps the stock price from exploding overnight.

Is the "Green Shift" Enough to Move the Needle?

You’ve probably heard that renewable energy is the future. For PFC, it’s the present. Their renewable portfolio grew by a staggering 32% in the first half of FY26. We’re talking about ₹85,000 crore already out the door for green projects.

They want renewables to make up 20% of their total loan book within three years. Right now, it’s closer to 13%. If they hit that 20% mark, the Power Finance Corporation Ltd stock price might finally get the "ESG premium" that private companies enjoy.

The NCD Factor

Just this week, PFC announced they’re raising up to ₹5,000 crore through Non-Convertible Debentures (NCDs).

Why should you care?

🔗 Read more: Canada Dollar to RS: Why Your Exchange Rate Just Changed

Because it shows they can still get cheap money from the debt market. When a lender can borrow for less and lend for more, their margins stay fat. PFC’s net margins are currently hovering around 49.5%. That’s a level of profitability most tech companies would kill for.

What Most People Get Wrong About PFC

A lot of retail investors treat PFC like a "proxy" for the government. They think if the government needs money, they'll just squeeze PFC. While it's true they pay out healthy dividends (like the ₹3.65 per share interim dividend declared in late 2025), the company is run much more like a commercial bank than a government department these days.

Also, don't confuse PFC with its sibling, REC Limited. They often move in tandem, but PFC has a slightly different exposure to large-scale generation projects.

The Numbers You Actually Need to Know

If you're trying to figure out if the current Power Finance Corporation Ltd stock price is a steal, look at these specific metrics:

- Price-to-Book (P/B): Around 1.04. Basically, you're buying the company’s assets at face value.

- Return on Equity (ROE): Approximately 19.7%.

- Target Prices: Most major analysts, including those from Motilal Oswal and ICICI Securities, have placed targets in the ₹480 to ₹500 range for late 2026.

Now, targets aren't guarantees. They’re educated guesses. But when the consensus is 30% higher than the current price, it usually means the fundamentals are disconnected from the daily noise.

Your Next Moves

Stop checking the price every ten minutes. It’s bad for your blood pressure and your strategy. If you’re looking at PFC, you’re likely an income investor or someone betting on India’s 2030 energy targets.

- Check the Q3 Results: Expect them around February. If the net NPA stays below 0.4%, the "bad debt" argument is officially dead.

- Monitor the Renewable Mix: Every time that percentage ticks up, the risk profile of the company goes down.

- Watch the Yield: If the price drops further but the dividend stays steady, your yield goes up. At a 5% yield, PFC becomes an alternative to a Fixed Deposit with much higher upside potential.

The Power Finance Corporation Ltd stock price isn't going to double in a week. It’s a slow-burn play. But with India set to become the world’s second-largest solar market by 2026, the company providing the cash for those solar panels is in a pretty sweet spot. Just make sure you're comfortable with the "PSU discount" that usually keeps these stocks from trading at crazy high multiples.