Buying a house in Canada feels like a sport where the rules change every single Tuesday. Honestly, if you’ve been watching the Bank of Montreal mortgage landscape lately, you know the vibe is tense. One day the five-year fixed is dropping, the next day inflation data from Statistics Canada spooked the bond market, and suddenly everyone is scrambling. People get obsessed with the "lowest" rate they see on a neon sign at a brokerage, but that’s rarely the rate they actually get.

BMO—or the Bank of Montreal, if we’re being formal—is the oldest bank in Canada. They’ve been doing this since 1817. That matters because, while fintech startups might have a flashy app, BMO has the balance sheet to weather the weirdness of the current economy. But here’s the thing: a BMO mortgage isn't just one thing. It’s a massive ecosystem of fixed-rate products, variables, and something called the Homeowner ReadiLine that confuses basically everyone until they see it in action.

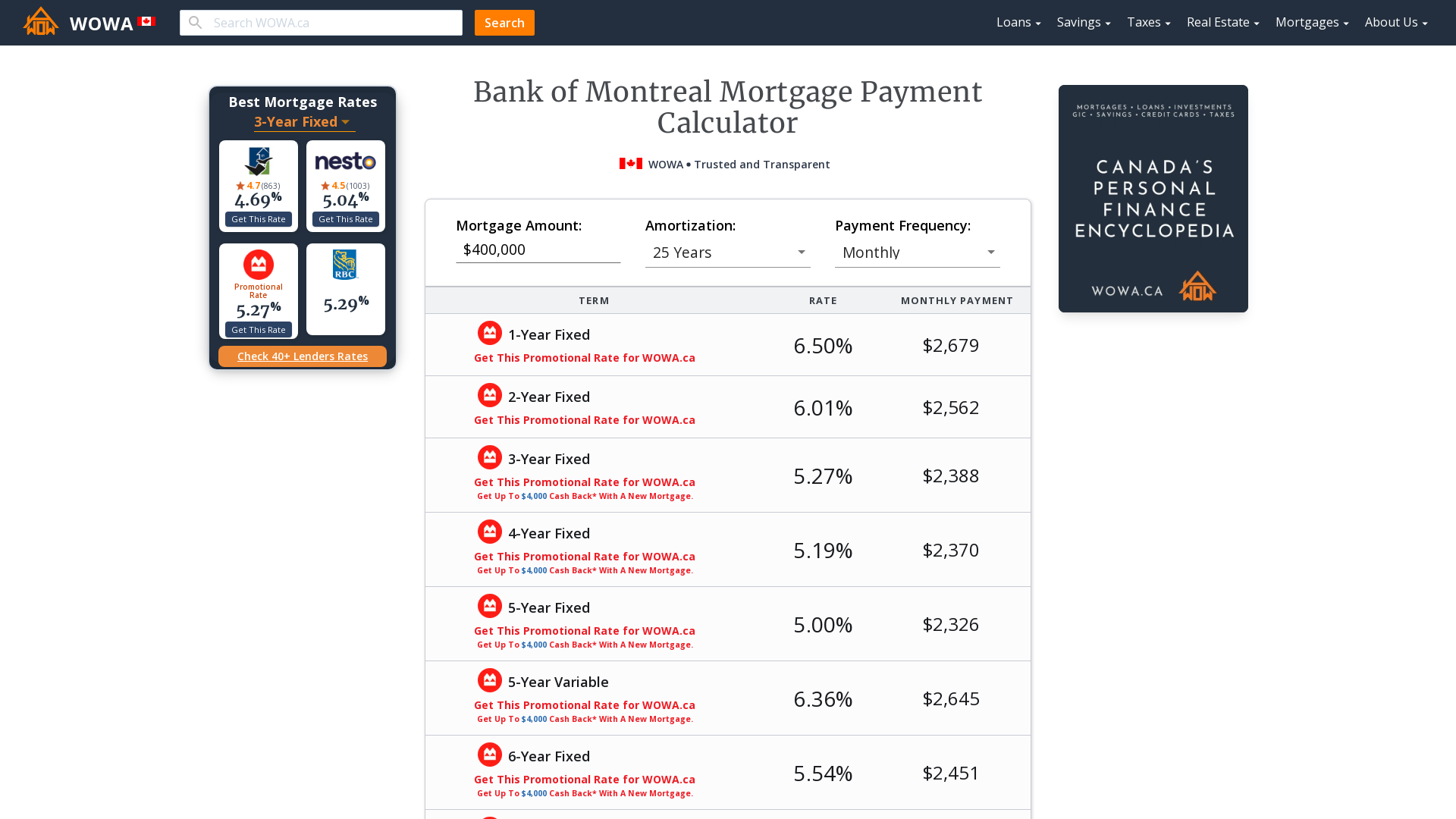

The Reality of BMO Mortgage Rates vs. The "Big Six"

Most people think all the big banks have the same rates. They don't. While the Bank of Canada sets the overnight rate—which directly dictates BMO’s prime rate—the way they price their fixed-rate mortgages depends on the bond market. Specifically the five-year Government of Canada bond yield.

If you walk into a branch on St-Jacques Street in Montreal or a tiny office in Red Deer, the "posted rate" you see is a lie. Okay, maybe not a lie, but it’s a placeholder. Nobody pays the posted rate. You’re looking for the "discretionary" or "special" rate. BMO is famous for its "Low Rate Fixed Term" mortgages. These are usually their "no-frills" options. You get a lower interest rate, but you lose some flexibility. For example, your ability to prepay large chunks of the principal might be capped at 10% instead of the 20% you'd get with a standard term.

Is it worth it?

Depends on if you’re a "set it and forget it" person or if you’re expecting a massive inheritance from an eccentric aunt next year. If you aren't planning on dumping huge amounts of extra cash into the mortgage, take the lower rate. Save the money.

The Smartest Move: The BMO Homeowner ReadiLine

If you want to understand why wealthy investors like BMO, you have to look at the Homeowner ReadiLine. It’s basically a hybrid. It combines a traditional mortgage with a Home Equity Line of Credit (HELOC).

Here’s how it works: as you pay down your mortgage principal, your credit limit on the HELOC side automatically increases. It’s like a see-saw. Mortgage goes down, available credit goes up. You don't have to re-apply. You don't have to beg a loan officer for money to fix your roof or buy a rental property. It’s just there.

But be careful.

The interest on the HELOC portion is usually Prime + 0.5%. If the Bank of Canada is feeling aggressive, that rate can climb fast. During the rate hikes of 2023 and 2024, a lot of people who were coasting on their ReadiLine suddenly realized their interest-only payments had doubled. It wasn't pretty.

Fixed vs. Variable: The 2026 Dilemma

We’re in a weird spot. For years, variable was the undisputed king. Then, the world broke. Now, most BMO clients are gravitating toward 3-year fixed terms. Why three years? Because five years feels like a lifetime in this economy, and one year is too risky. Three years is the "Goldilocks" zone.

- Fixed Rate: You know exactly what’s coming out of your bank account. No surprises. BMO’s 5-year fixed is the benchmark, but the 3-year is where the volume is shifting.

- Variable Rate: Your payment stays the same at BMO (usually), but the amount going toward your principal changes. If rates go up, you pay more interest and less principal. If they go high enough, you hit your "trigger point."

The trigger point is the boogeyman of Canadian real estate. It’s the moment your monthly payment doesn't even cover the interest. If that happens, BMO will call you. They’ll ask you to increase your payment or lump in a sum of cash. It’s a conversation nobody wants to have.

First-Time Home Buyers and the BMO "Starter" Experience

BMO has a soft spot for first-timers, or at least their marketing does. They offer a "First Home Fixed Rate Mortgage" which sometimes includes a slightly longer rate-hold period. Most banks give you 90 to 120 days. BMO has been known to stretch that, which is huge if you’re buying a pre-construction condo that keeps getting delayed.

👉 See also: IRS Code 150 With Future Date: Why Your Tax Transcript Looks Like It Is From The Future

You also need to talk about the stress test.

Even if BMO offers you a rate of 4.5%, the federal government (OSFI) says the bank has to check if you can handle roughly 6.5%. It feels unfair. It feels like they’re moving the goalposts. But it’s there to prevent a total housing collapse. When you’re applying at BMO, your "GDS" (Gross Debt Service) and "TDS" (Total Debt Service) ratios are the only numbers that actually matter to the underwriter. Keep your total debt—credit cards, car loans, and the new mortgage—under 42% of your gross income. If you’re at 43%, you’re probably getting a rejection letter, or at least a very awkward phone call.

The Nuance of Prepayment Charges

Nobody reads the fine print until they have to sell their house three years early because they got a job in London or decided they hate their spouse. BMO, like all the Big Six, uses an IRD (Interest Rate Differential) calculation for fixed-rate penalties.

This is where they get you.

The IRD isn't just the difference between your rate and the current rate. It’s often calculated using the posted rate at the time you signed, compared to the current rate for a term that matches your remaining time. It can cost you $20,000 to break a mortgage. If you think there’s even a 20% chance you’ll sell before your term is up, look into a variable rate. The penalty for breaking a variable mortgage is usually just three months of interest. That’s the difference between a $2,000 headache and a $20,000 catastrophe.

Comparing BMO to the "Online" Lenders

You’ll see ads for lenders like Rocket Mortgage or Questrade (QuestMortgage) offering rates that look significantly lower than BMO.

Why go with the big bank then?

Structure. If you have a complex income—maybe you’re self-employed or you have a side hustle as a consultant—online algorithms will often spit you out. BMO has actual humans (mortgage specialists) who can look at your tax returns and say, "Okay, I see what’s happening here." They have more "discretionary" power than an app. Plus, having your mortgage, checking account, and credit card in one place simplifies your life, even if you’re paying an extra 0.1% for the privilege.

Modern Features: The BMO PowerSwitch

BMO recently pushed a "PowerSwitch" program. It’s basically their way of aggressive poaching. If you have a mortgage at RBC or TD, BMO will often pay your appraisal fees and sometimes even give you a "switch cashback" to move to them. It’s worth checking if you’re at renewal. Never just sign the renewal paper your current bank sends you in the mail. That paper is the "lazy tax." They know most people won't shop around, so they offer a sub-optimal rate.

Actionable Steps for Your BMO Application

Stop guessing and start prepping.

- Pull your own credit report first. Use Equifax or TransUnion. If there’s an error—like a "late payment" from a gym membership you cancelled in 2022—fix it now. BMO’s automated system will flag a score below 680 as a "manual review," which slows everything down.

- Calculate your "Cash to Close." It’s not just the down payment. You need roughly 1.5% of the home’s price in cash for land transfer taxes, legal fees, and title insurance. BMO will want to see this money sitting in an account for at least 90 days.

- Ask for the "Standard Charge" vs "Collateral Charge" talk. BMO typically registers mortgages as collateral charges. This makes it easier to increase your loan later (like with the ReadiLine), but it makes it harder to switch to a different bank at the end of your term without paying legal fees. Know what you're signing.

- Negotiate. The first rate they give you is the "warm-up." Mention that you’re looking at Scotiabank or a local credit union. If your credit is good and your income is stable, the mortgage specialist has room to move. They want the volume.

The Canadian real estate market is a beast. Whether you’re looking at a bungalow in Etobicoke or a glass tower in Vancouver, the Bank of Montreal is a steady hand, but you have to be your own advocate. Don't fall for the glossy brochures. Look at the prepayment terms, understand the IRD penalty, and for heaven’s sake, make sure you actually like the person you’re dealing with. You’re going to be talking to them a lot.

Check your current debt-to-income ratio before you even book the appointment. If you're carrying a $600/month car payment, that could be the difference between getting the home you want and staying in your apartment for another two years. Clear the small debts first. It changes the math more than you think.